Generational Wealth Institute™

Foundational Framework Paper

Contents

- 1 Executive Summary

- 2 The Ownership Continuity Framework™

- 3 What Is Ownership Continuity?

- 4 Why Inheritance Is Not the Same as Continuity

- 5 Why Ownership Continuity Matters

- 6 The Ownership Continuity Chain™

- 7 The Four Continuity Layers

- 8 The Breakpoints of Generational Wealth

- 8.1 Breakpoint 1: Income Never Becomes Ownership

- 8.2 Breakpoint 2: Ownership Remains Scattered

- 8.3 Breakpoint 3: Structure Exists Without Governance

- 8.4 Breakpoint 4: Governance Exists Without Successor Preparation

- 8.5 Breakpoint 5: Transfer Happens Without Stewardship

- 8.6 Breakpoint 6: Ownership Fragments Across Generations

- 8.7 Breakpoint 7: The Founder’s Memory Becomes the System

- 8.8 Breakpoint 8: Ownership Purpose Is Lost

- 8.9 Why Breakpoints Matter

- 9 Income Formation: Wealth Must First Be Created

- 10 Ownership Formation: Income Must Become Ownership

- 11 Structure: Ownership Must Become Visible

- 12 Governance: Ownership Must Be Directed

- 13 Stewardship: Ownership Must Be Protected and Improved

- 14 Successor Preparation: Future Owners Must Be Prepared

- 15 Transfer: Ownership Must Move With Responsibility

- 16 Continuity: Ownership Must Survive Across Time

- 17 Ownership Capacity Across Generations

- 18 Continuity Governance Map

- 19 Reader Application

- 19.1 Can Your Ownership System Preserve Structure?

- 19.2 Can Your Ownership System Preserve Governance?

- 19.3 Can Your Ownership System Preserve Decision-Making Capacity?

- 19.4 Can Your Ownership System Preserve Stewardship?

- 19.5 Can Your Ownership System Preserve Successor Readiness?

- 19.6 Can Your Ownership System Preserve Purpose?

- 20 Ownership Continuity Readiness Questions

- 20.1 1. Can your ownership system survive beyond the founder?

- 20.2 2. Are assets clearly identified and organized?

- 20.3 3. Is ownership structure documented?

- 20.4 4. Are decision rights clear?

- 20.5 5. Is governance active?

- 20.6 6. Are successors being prepared?

- 20.7 7. Are roles across family members defined?

- 20.8 8. Is there a system for communication and conflict resolution?

- 20.9 9. Can ownership transfer without losing purpose?

- 20.10 10. Does the next generation understand what they are receiving?

- 21 Key Observations

- 21.1 Continuity is different from inheritance.

- 21.2 Ownership must become visible before it can be transferred well.

- 21.3 Governance protects ownership from fragmentation.

- 21.4 Structure alone is not enough.

- 21.5 Successors must be prepared before they receive control.

- 21.6 The founder’s memory is not a continuity system.

- 21.7 Ownership continuity requires both systems and people.

- 21.8 Generational wealth is preserved through continuity.

- 22 Conclusion

- 23 Frequently Asked Questions

- 23.1 What is ownership continuity?

- 23.2 Why is ownership continuity important?

- 23.3 What is the difference between inheritance and continuity?

- 23.4 How does ownership continuity support generational wealth?

- 23.5 What are the main parts of the Ownership Continuity Framework™?

- 23.6 Why is income not enough to build generational wealth?

- 23.7 Why does ownership need structure?

- 23.8 How does governance support ownership continuity?

- 23.9 What role does stewardship play in generational wealth?

- 23.10 Why must successors be prepared before ownership transfers?

- 23.11 How does business succession connect to ownership continuity?

- 23.12 How do holding companies connect to ownership continuity?

- 23.13 What causes generational wealth to break down?

- 23.14 Can a family transfer assets but still lose continuity?

- 23.15 What is ownership capacity?

- 23.16 How can families begin building ownership continuity?

- 23.17 Is ownership continuity the same as estate planning?

- 23.18 Does ownership continuity require a holding company?

- 23.19 Who should care about ownership continuity?

- 23.20 How does ownership continuity prepare future generations?

- 24 Related Institute Papers

- 24.1 Why Most Families Never Build Ownership: The Missing Link Between Income and Generational Wealth

- 24.2 What Is Family Governance? The Missing Layer in Most Wealth Plans

- 24.3 Family Wealth Transfer: Why Continuity Matters More Than Inheritance

- 24.4 Business Succession Planning: What Most Owners Miss About Ownership Transfer

- 24.5 What Is a Holding Company? A Framework for Long-Term Ownership

- 25 Authoritative Sources

Executive Summary

Generational wealth is often discussed as if the central challenge is transfer.

A family builds wealth.

A founder creates a business.

Assets accumulate.

Documents are prepared.

Beneficiaries are named.

Ownership eventually changes hands.

But transfer is not the same as continuity.

Assets can move from one generation to another while the deeper system of ownership weakens. A business can be passed down without transferring leadership judgment. Real estate can be inherited without a clear ownership structure. Financial assets can be divided without governance. Intellectual property can exist without stewardship. A family can receive wealth without understanding how to preserve, govern, improve, or responsibly direct it.

This is one of the central problems in generational wealth.

The issue is not only whether wealth can be transferred. The issue is whether ownership can continue.

Ownership continuity is the system that allows wealth to move across time without losing structure, governance, responsibility, or purpose.

This distinction matters because inheritance alone does not preserve generational wealth. Inheritance can move assets. Continuity preserves the capacity to own.

That capacity includes the ability to understand what is owned, how ownership is structured, who has authority, how decisions are made, how conflict is handled, how successors are prepared, how assets are stewarded, and how ownership responsibility is transferred over time.

Without continuity, wealth may fragment after transfer.

With continuity, ownership can remain structured, governed, stewarded, and prepared for future generations.

This paper introduces the Ownership Continuity Framework™ as a foundational model for understanding how wealth becomes durable across generations. The framework connects income formation, ownership formation, structure, governance, stewardship, successor preparation, transfer, and continuity.

Each layer matters.

Income must become ownership.

Ownership must become visible.

Structure must be governed.

Governance must support stewardship.

Stewardship must prepare successors.

Transfer must include responsibility.

Continuity must preserve ownership capacity across time.

This paper builds on the Institute’s prior ownership work. Earlier papers explained why income alone does not become generational wealth, why governance is the missing layer in many wealth plans, why continuity matters more than inheritance, why business succession is the transfer of responsibility, and why holding companies can help make ownership architecture visible.

This paper brings those ideas together.

The central argument is simple:

Generational wealth is not preserved by possession alone. It is preserved by continuity.

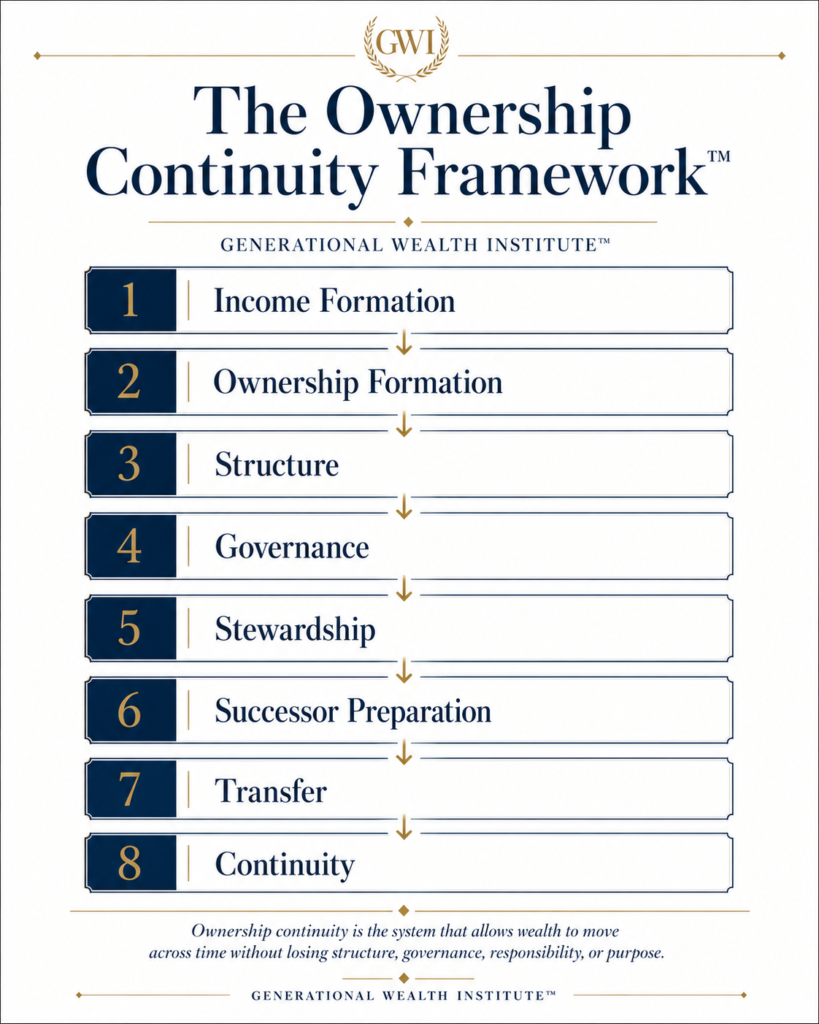

The Ownership Continuity Framework™

Ownership continuity can be understood through eight connected layers:

- Income Formation

- Ownership Formation

- Structure

- Governance

- Stewardship

- Successor Preparation

- Transfer

- Continuity

These layers are not isolated concepts. They form a sequence.

Income creates the possibility of ownership. Ownership gives income a durable form. Structure makes ownership visible. Governance directs ownership decisions. Stewardship protects and improves ownership over time. Successor preparation builds future ownership capacity. Transfer moves ownership responsibility. Continuity preserves the system across generations.

When one layer is missing, generational wealth becomes more fragile.

A family may have income but no ownership.

A family may have ownership but no structure.

A family may have structure but no governance.

A family may have governance documents but no prepared successors.

A family may transfer assets but fail to transfer responsibility.

A family may inherit wealth but lose the system required to preserve it.

This is why ownership continuity must be built intentionally.

It does not happen simply because assets exist.

What Is Ownership Continuity?

Ownership continuity is the process of building, organizing, governing, stewarding, preparing, and transferring ownership so that wealth can remain durable across generations.

It is not the same as inheritance.

It is not the same as estate planning.

It is not the same as having assets.

It is not the same as placing names on documents.

Ownership continuity asks a deeper question:

Can the ownership system survive beyond the person, generation, founder, or family member who built it?

That question changes the conversation.

Many wealth plans focus on what happens when assets transfer. Ownership continuity focuses on what must be built before transfer occurs.

It asks:

Are the assets clearly identified?

Is ownership visible?

Is the structure organized?

Are decision rights clear?

Is governance active?

Are successors being prepared?

Can family members communicate about ownership?

Can conflict be handled without destroying value?

Can the next generation understand what it is receiving?

Can ownership continue without depending entirely on one person?

These are not only legal or financial questions. They are ownership questions.

A family may have documents and still lack continuity. A business may have a succession plan and still remain founder-dependent. A real estate portfolio may be valuable but poorly organized. A holding company may exist but lack governance. A trust may hold assets but fail to prepare beneficiaries for responsibility.

Continuity requires more than transfer mechanics.

It requires ownership capacity.

Ownership Continuity Is the Preservation of Ownership Capacity

Ownership capacity is the ability to understand, govern, steward, and responsibly direct ownership.

It includes knowledge, judgment, structure, authority, communication, discipline, and responsibility.

A future owner does not have ownership capacity simply because they receive assets. Receiving wealth is not the same as being prepared to own it.

This is one reason many families struggle after transfer. The assets move, but the capacity to manage and govern those assets does not move with the same clarity.

For example, a founder may understand the business deeply because they built it. They know the customers, lenders, advisors, employees, risks, margins, informal relationships, and decision logic. But if that knowledge is never transferred, the next generation may inherit the company without inheriting the founder’s judgment on ownership.

The same pattern can happen with real estate.

A family may inherit properties but not understand financing, maintenance reserves, tenant risk, tax obligations, legal exposure, insurance, ownership agreements, or reinvestment strategy.

The asset transfers.

The ownership capacity does not.

Ownership continuity exists to close that gap.

Ownership Continuity Is Bigger Than Asset Transfer

Asset transfer is important, but it is only one part of continuity.

Transfer answers the question:

Who receives what?

Continuity asks:

Can what is received remain organized, governed, and stewarded over time?

That second question is much larger.

A family can transfer property to heirs. But if the heirs disagree about whether to sell, refinance, hold, improve, or divide the property, the ownership system may become unstable.

A founder can transfer shares in a company. But if there is no clear governance system, the next generation may fight over authority, distributions, leadership, reinvestment, compensation, or whether the business should continue.

Parents can leave financial assets to children. But if those children have not been prepared for responsibility, the inheritance may become consumption instead of continuity.

This does not mean transfer planning is unimportant.

It means transfer planning is incomplete if it does not address the system around ownership.

Ownership Continuity Requires Structure and People

Ownership continuity has two sides.

The first side is structural.

This includes entities, ownership maps, operating agreements, trusts, shareholder arrangements, governance policies, documentation, decision rights, advisor coordination, and legal architecture.

The second side is human.

This includes judgment, communication, stewardship, successor preparation, family maturity, role clarity, responsibility, and shared understanding.

Both sides are necessary.

Structure without prepared people can become mechanical and misunderstood.

People unprepared for structure can become frustrated and disorganized.

A serious ownership system needs both.

For example, a holding company may help consolidate multiple assets under a single ownership layer. But the holding company itself does not decide family values, prepare successors, resolve disputes, establish distribution discipline, or teach future owners how to steward wealth.

Likewise, a family may have strong values and good intentions but still lack the structural tools needed to organize business interests, real estate, investments, intellectual property, or future acquisitions.

Continuity emerges when ownership structure and human capacity work together.

A Simple Definition

Ownership continuity is the system that helps ownership move across time without losing structure, governance, responsibility, stewardship, or purpose.

It is the bridge between building wealth and preserving wealth.

It is the difference between handing down assets and preparing ownership to survive.

Why Inheritance Is Not the Same as Continuity

[Insert Infographic 2: Inheritance vs. Continuity]

Inheritance and continuity are often treated as if they are the same thing.

They are not.

Inheritance is usually event-based. It happens when assets, rights, or property interests pass from one person to another, often after death or through a planned transfer.

Continuity is system-based. It exists when ownership remains organized, governed, stewarded, and capable across time.

The difference is critical.

A person can inherit assets without understanding ownership.

A family can inherit wealth without governance.

A child can inherit shares without decision-making capacity.

Siblings can inherit property without a conflict-resolution process.

A business can transfer legally without transferring leadership responsibility.

Inheritance answers the question of receipt.

Continuity answers the question of survival.

Inheritance Moves Assets

Inheritance can move assets from one generation to another.

Those assets may include real estate, business interests, cash, investments, intellectual property, land, personal property, or other forms of wealth.

This movement matters. Without some form of transfer, ownership cannot pass to future generations.

But inheritance alone does not guarantee that assets will remain productive, protected, coordinated, or aligned with long-term purpose.

A family may inherit a rental property but disagree on whether to hold or sell it.

A family may inherit a business but lack leadership readiness.

A family may inherit financial assets but lack investment discipline.

A family may inherit land but lack governance around use, development, sale, or preservation.

The inheritance occurs.

The ownership system may still fail.

Continuity Preserves Ownership Capacity

Continuity is concerned with what happens after receipt.

It asks whether the next owner or ownership group has the capacity to preserve, govern, and responsibly direct what has been transferred.

That capacity includes practical knowledge.

What is owned?

Where is it held?

Who has authority?

What obligations come with it?

What risks exist?

What agreements govern it?

Who advises the family?

How are decisions made?

How are conflicts handled?

How are future owners prepared?

When those questions are unanswered, inheritance can create confusion.

When those questions are addressed before transfer, inheritance becomes part of continuity rather than a fragile event.

Assets Can Transfer Without Understanding

One of the most dangerous assumptions about generational wealth is that receiving an asset means understanding it.

That is rarely true.

A beneficiary may receive ownership interests without understanding voting rights.

An heir may receive real estate without understanding debt, maintenance, insurance, taxes, or liquidity needs.

A child may receive a business interest without understanding the difference between ownership, management, employment, and distributions.

A family member may receive trust benefits without understanding the purpose of the trust, the role of trustees, or the long-term stewardship responsibility behind the structure.

This gap between receipt and understanding is where continuity often breaks.

The asset arrives.

The responsibility is unclear.

Transfer Without Continuity Can Create Fragility

Transfer can create fragility when assets move into an unprepared ownership system.

The first generation may be able to hold everything together through personal authority, memory, relationships, or control.

But after the transfer, the system changes.

More people may become owners.

Decision-making may become shared.

Different expectations may emerge.

Liquidity needs may diverge.

Family relationships may affect business decisions.

Some heirs may work in the business while others do not.

Some may want income. Others may want reinvestment.

Some may want to sell. Others may want to preserve.

Without governance, these differences can become destructive.

This is why continuity must be built before transfer.

Inheritance moves assets.

Continuity preserves ownership.

Why Ownership Continuity Matters

Ownership continuity matters because generational wealth often fails at the level of system, not only at the level of asset value.

A family may lose wealth because an investment performs poorly.

But families also lose wealth because ownership becomes fragmented, governance is unclear, successors are unprepared, the founder remains the only source of knowledge, or assets are transferred without structure.

These are continuity failures.

They are not always visible at first.

A family may appear wealthy because it owns assets. But if the ownership structure is unclear, decision-making is informal, successors are unprepared, and conflict is unresolved, that wealth may already be fragile.

The appearance of wealth can hide the absence of continuity.

Wealth Can Be Lost Through Fragmentation

Fragmentation occurs when ownership is spread among people, entities, assets, and generations without a coordinating system.

This can happen slowly.

A founder owns a business directly.

Then shares are passed to children.

Then children marry, divorce, relocate, or develop different goals.

Then, grandchildren enter the picture.

Then some owners work in the business, and others do not.

Then some want income, and others want reinvestment.

Then no one agrees who has authority.

The business may still exist, but ownership becomes harder to coordinate.

Fragmentation also happens outside business ownership.

A family may own multiple properties, small investment accounts, informal loans, intellectual property, vehicles, or land interests. If no one maintains a clear ownership map, the family may not even fully understand what it owns.

When ownership is scattered, continuity weakens.

Wealth Can Be Lost Through Lack of Governance

Governance is the decision-making system that keeps ownership coordinated across time.

Without governance, families often rely on personality, informal authority, assumptions, or the founder’s memory.

That may work temporarily.

It rarely works across generations.

Governance clarifies:

who makes decisions

who has authority

how meetings happen

how information is shared

how distributions are decided

how reinvestment is evaluated

how conflict is handled

how successors enter decision-making

how advisors are coordinated

how ownership purpose is preserved

Without governance, ownership can become emotionally overloaded.

Every financial decision can become a family conflict.

Every business decision can become a loyalty test.

Every distribution decision can become a fairness debate.

Every succession decision can become a personal wound.

Governance does not eliminate disagreement.

It gives disagreement a structure.

Wealth Can Be Lost Through Unprepared Successors

Future owners need preparation before they receive control.

This does not mean every heir must become an operator, investor, trustee, executive, or manager.

It means future owners should understand what ownership requires.

They should understand the assets.

They should understand the structure.

They should understand the governance system.

They should understand risk.

They should understand stewardship.

They should understand their role.

They should understand what decisions they are prepared to make and what decisions require advisors or governance bodies.

Without preparation, the next generation may inherit control before developing judgment.

That is dangerous.

Control without capacity can damage what prior generations built.

Wealth Can Be Lost Through Founder Dependence

Founder dependence occurs when the founder remains the center of knowledge, authority, relationships, judgment, and decision-making.

This is common in family businesses and entrepreneurial families.

The founder knows the bank.

The founder knows the attorney.

The founder knows the accountant.

The founder knows the customers.

The founder knows which employee can be trusted.

The founder knows the history behind every major decision.

The founder knows where the risk lies.

The founder knows which assets matter most.

But if that knowledge is not transferred, the ownership system remains fragile.

The founder may believe they have built wealth.

But in reality, they may have built wealth that still depends heavily on them.

Ownership continuity requires moving critical knowledge out of one person’s head and into a structured system that others can understand, govern, and steward.

Wealth Can Be Lost Through Unstructured Assets

Assets that are not organized become harder to govern and transfer.

This is why ownership structure matters.

A family may own assets directly, informally, or across multiple disconnected accounts and entities. Over time, this can make ownership harder to understand.

Who owns what?

Which entity holds which asset?

Which agreements apply?

Who has authority?

Which assets produce income?

Which assets require capital?

Which assets are strategic?

Which assets are sentimental?

Which assets should be preserved, sold, improved, or transferred?

If the family cannot answer these questions clearly, continuity becomes difficult.

Structure makes ownership visible.

Visibility makes governance possible.

Governance makes continuity more likely.

The Ownership Continuity Chain™

[Insert Infographic 3: The Ownership Continuity Chain™]

Ownership continuity does not happen through one decision, one document, one transfer, or one event.

It happens through a chain.

Each link supports the next. When one link is weak, the entire ownership system becomes more vulnerable.

The Ownership Continuity Chain™ includes eight connected links:

Income

Ownership

Structure

Governance

Stewardship

Successor Capacity

Transfer

Continuity

This chain helps explain why many families struggle to preserve wealth even when assets exist. The problem is rarely one single failure. More often, continuity breaks because one or more parts of the ownership chain were never built, never clarified, or never transferred.

A family may generate income but never convert it into durable ownership.

A family may own assets but fail to organize them.

A family may create entities but fail to govern them.

A family may have governance documents but no prepared successors.

A family may transfer wealth but fail to transfer responsibility.

Each missing link weakens continuity.

The chain matters because generational wealth is not simply about having assets. It is about whether ownership can remain functional across time.

Income Must Become Ownership

Income is often the starting point of wealth creation.

Families earn income through employment, professional work, business activity, entrepreneurship, investments, services, or enterprise building. But income by itself is temporary. It arrives, gets spent, gets taxed, gets consumed, or gets reinvested.

Income becomes generationally meaningful when it is converted into ownership.

That conversion may happen through business equity, real estate, financial assets, intellectual property, private investments, land, or other durable assets.

This is one of the Institute’s foundational ideas:

Income is not wealth until it becomes structure.

A family that earns well but owns little may appear financially successful while remaining structurally fragile. A high income can support lifestyle, but it does not automatically create continuity. If income stops and there are no durable ownership positions, the wealth system may weaken quickly.

Ownership gives income a longer life.

It allows value to exist beyond the earning moment.

Ownership Must Become Structured

Ownership alone is not enough.

A person can own assets and still lack an ownership system.

This happens when assets are scattered across personal accounts, informal arrangements, disconnected entities, undocumented agreements, family assumptions, or founder memory.

At first, this may not seem like a problem. One person may understand everything. The founder knows what is owned, where it sits, who manages it, which advisor to call, what risks exist, and why certain decisions were made.

But as assets grow, family members multiply, businesses expand, or generations change, informal ownership becomes harder to manage.

Structure makes ownership visible.

It helps answer basic but essential questions:

What is owned?

Who owns it?

Where is it held?

Which assets are operating assets?

Which assets are investment assets?

Which assets are personal, family, business, or strategic assets?

Which agreements control ownership?

How does cash move?

Who has authority?

Holding companies, trusts, operating entities, shareholder agreements, partnership structures, ownership maps, and governance documents may all play a role depending on the family, business, asset base, and legal context.

The specific structure must be designed by qualified professionals.

But the ownership principle is broader:

If ownership is not visible, it becomes harder to govern.

Structure Must Be Governed

Structure creates order, but structure does not govern itself.

A holding company can organize ownership.

A trust can hold assets.

An operating agreement can define rights.

A shareholder agreement can clarify ownership terms.

A board can exist on paper.

But none of these automatically creates healthy decision-making.

Governance is the system that directs ownership.

It answers questions such as:

Who makes decisions?

Who has authority?

Who receives information?

How are major decisions approved?

How are distributions handled?

How are conflicts resolved?

How are successors prepared?

How are advisors coordinated?

How are owners held accountable?

This is where ownership continuity becomes serious.

The OECD’s corporate governance principles frame governance as a legal, regulatory, and institutional framework that supports efficient markets, shareholder rights, disclosure, board responsibilities, sustainability, and resilience. While those principles are written for corporate governance at a broader institutional level, the underlying idea is directly relevant here: ownership requires a framework for authority, rights, responsibility, transparency, oversight, and long-term decision-making.

For family enterprises, the need is even more personal. The IFC Family Business Governance Handbook describes family business governance as a practical set of components and approaches for resolving common family business governance dilemmas, including family roles, board structure, employment policies, and succession planning.

For our purposes, the Institute principle is clear:

Structure without governance becomes confusion.

Governance Must Support Stewardship

Governance is not only about control.

It is also about stewardship.

Stewardship asks how ownership should be protected, improved, disciplined, and passed forward.

A family can have governance and still lack stewardship if decisions are driven only by short-term consumption, emotional pressure, status, entitlement, or avoidance.

Stewardship brings a different posture.

It asks:

What are we responsible for preserving?

What should be improved before it is transferred?

What risks must be managed?

What should be reinvested?

What should be distributed?

What should not be sold casually?

What values should guide ownership?

What obligations do current owners have to future owners?

Stewardship changes the identity of ownership.

The owner is not merely a receiver of benefit. The owner becomes a caretaker of value across time.

This matters because generational wealth is not only weakened by bad investments. It can also be weakened by poor stewardship, over-distribution, unmanaged conflict, unclear purpose, or failure to prepare the next generation.

Governance provides the decision-making system.

Stewardship provides the responsibility standard.

Stewardship Must Prepare Successors

Ownership continuity cannot depend only on current owners.

At some point, ownership must pass to future owners.

That means stewardship must include preparation.

Successor preparation is not simply telling heirs that they will receive assets one day. It is the process of helping future owners understand ownership before control arrives.

That preparation may include:

financial education

business exposure

family history

governance participation

advisor introductions

decision-making practice

risk education

role clarity

stewardship expectations

conflict-management norms

understanding of entities and documents

knowledge of family assets and obligations

This preparation is especially important in family enterprises, where ownership, family relationships, employment, control, and identity often overlap. IFC’s family business governance materials specifically emphasize governance structures, family roles, employment policies, board structure, and succession planning as part of family business continuity.

In Institute language:

Future owners must be prepared before ownership is transferred.

If preparation begins only after transfer, continuity is already under stress.

Transfer Must Preserve Responsibility

Transfer is one of the most visible moments in generational wealth.

It is also one of the most misunderstood.

Many families focus on who receives what.

But ownership continuity asks whether responsibility transfers with the asset.

Responsibility includes:

knowledge

authority

decision-making capacity

governance participation

stewardship expectations

understanding of risk

respect for purpose

ability to work with advisors

ability to coordinate with other owners

When assets transfer without responsibility, the ownership system becomes fragile.

A business interest may transfer, but no one understands how the business makes money.

A property may transfer, but no one understands capital needs.

A trust may benefit heirs, but beneficiaries do not understand its purpose.

A holding company may exist, but family members do not understand its role.

A portfolio may transfer, but no one knows the investment philosophy.

The result is transfer without continuity.

That is why transfer must be treated as a process, not only an event.

Continuity Requires the Whole Chain

Ownership continuity depends on the whole chain.

Income must become ownership.

Ownership must become structured.

Structure must be governed.

Governance must support stewardship.

Stewardship must prepare successors.

Successors must receive responsibility, not only assets.

Transfer must preserve the system.

Continuity must be renewed by each generation.

This is why one isolated solution is never enough.

A trust alone does not create continuity.

A will alone does not create continuity.

A holding company alone does not create continuity.

A family meeting alone does not create continuity.

A succession document alone does not create continuity.

A financial portfolio alone does not create continuity.

Each tool can matter.

But continuity requires the tools to work inside a broader ownership system.

Generational wealth weakens when one link in the ownership continuity chain breaks.

The Four Continuity Layers

[Insert Infographic 4: The Four Continuity Layers]

Ownership continuity can also be understood through four layers:

The Asset Layer

The Structure Layer

The Governance Layer

The Human Capacity Layer

These layers help explain why assets alone are not enough.

A family may own valuable assets, but if those assets are not structured, governed, or stewarded by prepared people, continuity remains fragile.

Each layer plays a different role.

The Asset Layer answers: What is owned?

The Structure Layer answers: How is ownership organized?

The Governance Layer answers: How are decisions made?

The Human Capacity Layer answers: Who is prepared to carry responsibility forward?

A serious ownership system needs all four.

The Asset Layer

The Asset Layer includes what the family, founder, business, or ownership group actually owns.

This may include:

operating businesses

real estate

land

financial assets

intellectual property

private investments

equipment

royalties

brand assets

digital assets

cash reserves

ownership interests

family enterprise assets

The Asset Layer matters because continuity cannot exist in the abstract. Something must be owned, preserved, improved, governed, or transferred.

But assets alone do not create continuity.

A family may own real estate and still disagree about whether to sell.

A founder may own a business and still have no succession system.

A family may own investment accounts and still lack shared purpose.

A company may own intellectual property and still lack a plan for who controls or commercializes it.

Assets are the foundation.

They are not the full system.

The Structure Layer

The Structure Layer organizes ownership.

This is where ownership becomes visible, documented, and easier to govern.

Depending on the context, the Structure Layer may include:

holding companies

operating companies

trusts

limited liability entities

partnerships

shareholder agreements

operating agreements

ownership maps

estate documents

buy-sell agreements

family investment entities

asset-holding entities

intellectual property entities

real estate entities

governance charters

The purpose of structure is not complexity for its own sake.

The purpose is clarity.

Structure helps show where assets sit, who owns them, who controls them, how value flows, how decisions are made, and how ownership may eventually transfer.

But structure should follow purpose.

A family should not create entities simply because sophisticated families use entities. A founder should not create a holding company simply because it sounds powerful. A business owner should not assume that structure automatically creates protection, tax benefit, or continuity.

Structure must be appropriate, professionally designed, and connected to the owner’s actual goals.

The Institute principle is:

Ownership must become visible before it can be transferred well.

The Governance Layer

The Governance Layer directs ownership.

This layer determines how decisions are made, reviewed, communicated, and enforced.

It may include:

family councils

boards

advisory boards

trustees

ownership meetings

family constitutions

distribution policies

investment policies

employment policies

succession policies

conflict-resolution processes

advisor coordination

reporting standards

decision rights

voting procedures

role definitions

Governance is the difference between ownership as possession and ownership as organized responsibility.

The OECD’s corporate governance principles emphasize the importance of frameworks that support shareholder rights, equitable treatment, disclosure, board responsibilities, sustainability, and resilience. These principles reinforce the broader point that ownership works better when rights, responsibilities, transparency, and oversight are structured rather than assumed.

In a family context, governance is especially important because family relationships can complicate ownership decisions.

A sibling disagreement may become a business problem.

A distribution decision may become a fairness argument.

A leadership transition may become a family identity crisis.

A reinvestment decision may expose different risk tolerances.

A sale decision may divide emotional and financial priorities.

Governance does not remove emotion from ownership.

It gives ownership a process strong enough to carry emotion without collapsing.

The Human Capacity Layer

The Human Capacity Layer is the most overlooked layer.

It includes the people who must understand, govern, steward, and eventually continue ownership.

This layer includes:

prepared successors

responsible owners

educated beneficiaries

capable operators

trusted advisors

family leaders

board members

trustees

next-generation participants

stewards of family purpose

Many families overbuild the structural layer and underbuild the human capacity layer.

They create documents, entities, trusts, companies, and legal structures, but they do not prepare the people who must live inside those structures.

That creates a dangerous gap.

The structure may be technically sound, but the people may be unprepared.

They may not understand the purpose of the structure.

They may not know how decisions are supposed to be made.

They may not understand the assets.

They may not know their roles.

They may not trust each other.

They may not know how to work with advisors.

They may not understand stewardship.

Ownership continuity depends on people, not only paperwork.

The human layer is where ownership becomes lived responsibility.

Why All Four Layers Matter

Each continuity layer supports the others.

The Asset Layer provides value.

The Structure Layer organizes value.

The Governance Layer directs value.

The Human Capacity Layer carries responsibility for value.

If the Asset Layer is weak, there may be little to preserve.

If the Structure Layer is weak, ownership may become scattered.

If the Governance Layer is weak, decisions may become unstable.

If the Human Capacity Layer is weak, future owners may be unable to steward what they receive.

This is why ownership continuity cannot be reduced to one professional document, one family conversation, one business structure, or one transfer event.

Assets do not preserve themselves.

Continuity requires structure, governance, and prepared people.

The Breakpoints of Generational Wealth

[Insert Infographic 5: The Breakpoints of Generational Wealth]

Generational wealth often breaks at predictable points.

These breakpoints are not always dramatic. They may appear slowly, quietly, and almost invisibly.

A family earns well but never builds ownership.

A founder builds a business but never reduces founder dependence.

A parent creates wealth but never prepares heirs.

A family owns assets but never creates governance.

A holding company exists but no one understands its purpose.

A trust exists but beneficiaries are not prepared for stewardship.

A family inherits property but cannot agree what to do with it.

The wealth may still exist on paper.

But continuity may already be weakening.

A breakpoint is a place where ownership loses structure, governance, knowledge, responsibility, or prepared successors.

The more breakpoints a family has, the more fragile its wealth becomes.

Breakpoint 1: Income Never Becomes Ownership

The first breakpoint occurs when income never becomes ownership.

This is one of the most common failure points.

A person may earn a strong income for years. A family may live well. A professional may build status. An entrepreneur may generate revenue. But if that income is not converted into assets, ownership, equity, or durable structures, it may not become generational wealth.

Income supports the present.

Ownership can support the future.

This does not mean every dollar should be invested or every family must build a complex ownership system. It means that without some disciplined conversion from income to ownership, wealth may not survive beyond the earning capacity of the individual.

The family may have lifestyle but no structure.

That is a fragile position.

Breakpoint 2: Ownership Remains Scattered

The second breakpoint occurs when ownership exists but remains scattered.

This can happen when assets are acquired over time without an organizing architecture.

One property is held personally.

Another is held through an entity.

A business is owned directly.

An investment account is separate.

Intellectual property is undocumented.

Family loans are informal.

Insurance, estate documents, and business agreements do not align.

No one has a full ownership map.

At first, scattered ownership may not seem like a major problem.

But over time, it creates confusion.

The family may not know what it owns, who controls it, what obligations exist, what risks are hidden, or how assets should eventually transfer.

Scattered ownership becomes especially dangerous after death, disability, divorce, conflict, business transition, creditor pressure, or family disagreement.

Continuity requires ownership visibility.

Breakpoint 3: Structure Exists Without Governance

The third breakpoint occurs when a family has legal or ownership structures but lacks governance.

This is common among families that have received professional planning but have not built an active decision-making system.

They may have:

trusts

companies

operating agreements

estate documents

holding entities

tax planning structures

ownership agreements

But no clear governance rhythm.

No regular ownership meetings.

No decision process.

No communication norms.

No conflict-resolution process.

No role clarity.

No successor education.

No shared understanding of purpose.

In this situation, structure may create the appearance of readiness.

But when a real decision arises, confusion appears.

Who decides whether to sell?

Who has authority to reinvest?

Who speaks with advisors?

Who explains the structure to the next generation?

Who resolves disagreement?

Who protects the purpose of the assets?

If those questions are unanswered, structure alone is not enough.

Structure without governance becomes confusion.

Breakpoint 4: Governance Exists Without Successor Preparation

The fourth breakpoint occurs when governance exists but successors are not prepared.

This can happen in families that have meetings, policies, advisors, and documents, but where the next generation is still passive or excluded.

The current owners may make decisions.

The advisors may understand the structure.

The founder may know the asset history.

The parents may understand the family purpose.

But future owners may remain uninformed.

They may know wealth exists, but not how it works.

They may know they are beneficiaries, but not what responsibility means.

They may know there is a family business, but not how ownership differs from employment.

They may know there are advisors, but not how to evaluate advice.

They may know assets will transfer, but not how to govern them.

This creates a delayed failure.

Everything may look orderly while the current generation is active.

Then transfer happens.

Suddenly the next generation must make decisions it was never prepared to make.

Governance without prepared successors becomes delay, confusion, or conflict.

Breakpoint 5: Transfer Happens Without Stewardship

The fifth breakpoint occurs when transfer happens without stewardship.

This is when assets move, but the deeper responsibility does not.

The next generation receives wealth but does not understand what the wealth is for.

They receive control but not discipline.

They receive benefits but not responsibility.

They receive access but not stewardship identity.

They receive ownership but not purpose.

This is dangerous because wealth without stewardship can become consumption, entitlement, fragmentation, or conflict.

Stewardship gives ownership a time horizon.

It teaches current and future owners to ask:

What did we receive?

What are we responsible for?

What must we preserve?

What must we improve?

What should we not damage?

What do future generations need from us?

What decisions would strengthen continuity?

Without stewardship, transfer can become extraction.

With stewardship, transfer can become continuity.

Breakpoint 6: Ownership Fragments Across Generations

The sixth breakpoint occurs when ownership fragments across generations.

This is one of the most difficult stages.

Generation 1 may build the asset.

Generation 2 may inherit or manage it.

Generation 3 may become more distant from the founder’s story, more numerous, more diverse in interests, and less emotionally connected to the original asset.

This pattern is common in family businesses and family-owned assets.

As generations expand, the ownership group becomes more complex.

There may be more spouses, cousins, branches, locations, financial needs, education levels, professional backgrounds, and expectations.

Some family members may work in the business.

Some may only own.

Some may want liquidity.

Some may want preservation.

Some may want growth.

Some may feel excluded.

Some may feel overburdened.

Some may not understand the history.

Without governance and stewardship, ownership can become harder to hold together.

Fragmentation does not always mean the family did something wrong.

It means the ownership system must mature as the family expands.

If the system does not mature, the assets may eventually be sold, divided, neglected, or fought over.

Breakpoint 7: The Founder’s Memory Becomes the System

Another major breakpoint occurs when the founder’s memory is treated as the ownership system.

This is especially common in founder-led businesses, entrepreneurial families, and first-generation wealth creation.

The founder remembers everything.

They remember why the property was purchased.

They remember which advisor drafted the documents.

They remember the handshake agreement.

They remember the lender relationship.

They remember the employee who should never be promoted.

They remember the customer who pays late but always pays.

They remember the real reason the family kept one asset and sold another.

They remember which sibling was promised what.

But memory is not continuity.

If the system exists only in the founder’s head, the system is not transferable.

Ownership continuity requires converting founder memory into shared knowledge, documented structure, governance processes, successor education, advisor coordination, and decision records.

The founder’s memory may be valuable.

But it cannot be the only map.

Breakpoint 8: Ownership Purpose Is Lost

The final breakpoint is loss of purpose.

A family may have assets, documents, governance, and successors, but still lose continuity if the deeper purpose of ownership disappears.

Purpose answers:

Why do we own this?

What are we building?

What should this wealth support?

What responsibilities come with it?

What should be preserved?

What should change?

What do we owe to future generations?

What should ownership make possible?

Without purpose, ownership can become purely transactional.

The family may eventually ask:

Why are we holding this business?

Why not sell the land?

Why stay connected?

Why preserve the structure?

Why reinvest?

Why make sacrifices for future owners?

Purpose does not mean every asset must be held forever.

Sometimes stewardship requires sale, restructuring, professionalization, or reallocation.

But without purpose, ownership decisions become reactive.

Continuity requires a reason to continue.

Why Breakpoints Matter

Breakpoints matter because they help families identify where continuity is most vulnerable.

Some families have an income problem.

Some have an ownership problem.

Some have a structural problem.

Some have a governance problem.

Some have a successor preparation problem.

Some have a stewardship problem.

Some have a transfer problem.

Some have a purpose problem.

The solution depends on the breakpoint.

A family that lacks ownership does not need a complex governance system yet. It first needs to convert income into assets.

A family with multiple entities but no decision process does not need more complexity. It needs governance.

A family with strong assets and strong structure but unprepared heirs does not need only estate documents. It needs successor preparation.

A founder-led business that depends entirely on one person does not need a ceremonial succession plan. It needs a responsibility transfer system.

The point is not to make every family follow the same path.

The point is to diagnose where ownership continuity is breaking.

Wealth often fails between generations because ownership capacity does not transfer with the assets.

Income Formation: Wealth Must First Be Created

Ownership continuity begins before ownership exists.

It begins with income formation.

This may seem obvious, but it matters because many conversations about generational wealth begin too late. They begin with inheritance, trusts, estate documents, family offices, holding companies, tax planning, or business succession.

Those things may matter.

But before wealth can be transferred, structured, governed, or preserved, it must first be created.

Income formation is the starting point because income creates the surplus from which ownership can emerge.

A person earns income.

A family creates surplus.

A business produces profit.

An operator generates cash flow.

A professional converts skill into compensation.

An entrepreneur converts risk into enterprise value.

That income becomes the raw material for ownership.

But income by itself is not continuity.

Income is active. It usually depends on work, time, effort, skill, employment, business performance, client relationships, sales, or market demand. It may be strong for a season and disappear later. It may support a household but fail to create transferable value. It may produce comfort without creating durable ownership.

This is why income formation is only the first layer.

Income creates possibility.

Ownership creates durability.

Income Is the Starting Point, Not the Destination

Many families confuse income success with wealth structure.

This is understandable.

Income is visible. It affects lifestyle immediately. It pays bills, funds education, supports housing, creates status, and provides comfort. When income rises, the family may feel that it is building wealth.

But income and wealth are not the same.

A family can have high income and still have weak ownership.

A professional can earn well and still own little.

A business owner can generate revenue and still have poor transferable value.

A household can appear financially successful while remaining dependent on continued earnings.

Income supports the present.

Ownership supports the future.

This does not mean income is unimportant. Income is essential. Without it, many families cannot create surplus, acquire assets, invest, build businesses, or make long-term ownership decisions.

But income must be treated as a source, not the final goal.

If income is consumed entirely, it ends with the earning period.

If income is converted into ownership, it can become part of a longer continuity system.

Income Must Be Converted Into Assets

The first major transition in generational wealth is the movement from income to assets.

This transition may happen gradually.

A family saves.

A household reduces unnecessary consumption.

A business owner reinvests profit.

A professional purchases equity-producing assets.

An entrepreneur builds enterprise value.

An investor accumulates ownership positions.

A creator protects intellectual property.

Over time, income begins to take a durable form.

It becomes something that can be owned, improved, governed, transferred, or stewarded.

This conversion matters because assets can outlast the original income stream.

A rental property can continue producing income after the original buyer stops working.

A business can continue generating value beyond the founder’s direct labor if it has systems, management, customers, governance, and transferable operations.

A portfolio can continue compounding if it is responsibly managed.

Intellectual property can continue producing value if it is protected, commercialized, and governed.

Ownership gives income a second life.

Income Without Ownership Does Not Become Continuity

Income without ownership may support a good life, but it rarely creates continuity by itself.

This is one of the most important distinctions for first-generation builders.

A person may earn enough to support a family, send children to school, buy a home, travel, help relatives, and live comfortably. These are meaningful accomplishments.

But if the income never becomes ownership, the family may remain vulnerable once the income stops.

The earning person retires.

The business slows down.

The job ends.

The professional loses capacity.

The market changes.

Health changes.

Demand changes.

If no ownership base has been built, the family’s financial position may weaken quickly.

This is why generational wealth requires conversion.

Income must be converted into something that can survive the income source.

That conversion is not automatic.

It requires discipline.

Income Formation Requires Discipline

Income formation requires more than earning.

It requires the discipline to turn income into surplus and surplus into ownership.

This may involve:

spending restraint

savings discipline

investment planning

business reinvestment

debt management

skill development

cash-flow tracking

tax awareness

risk management

insurance planning

strategic allocation

long-term thinking

For families trying to build generational wealth, the key question is not only:

How much do we earn?

The deeper question is:

What does our income become?

If income becomes only lifestyle, it may not create continuity.

If income becomes ownership, it can begin the generational wealth process.

Income is the seed.

Ownership is the structure that allows the seed to keep growing.

Ownership Formation: Income Must Become Ownership

Ownership formation is the point where income begins to become durable.

This is where the family, founder, business owner, or professional moves from earning to owning.

That move is central to generational wealth.

Without ownership, wealth has no durable container. Without ownership, income may support consumption but fail to create assets that can be governed, improved, or transferred. Without ownership, the next generation may receive memories, values, and education, but not an ownership system.

Ownership formation is the process of creating, acquiring, building, or organizing assets that can hold value beyond the earning period.

It is the first structural move in the continuity chain.

Ownership Gives Income a Durable Form

Income is temporary unless it is converted.

Ownership gives income a durable form.

A business interest can hold enterprise value.

A property can hold real asset value.

A portfolio can hold financial value.

Intellectual property can hold creative or commercial value.

A brand can hold reputational value.

A family enterprise can hold operating value.

When income becomes ownership, it becomes something that can be mapped, managed, governed, protected, improved, and eventually transferred.

This does not mean ownership is risk-free.

Every form of ownership carries risk. Businesses can fail. Property values can decline. Investments can lose value. Intellectual property can lose relevance. Private assets can become illiquid. Concentrated ownership can expose a family to significant vulnerability.

But without ownership, there is no durable wealth base to continue.

Continuity requires something that can be stewarded.

The Four Ownership Domains

Ownership can take many forms, but four broad domains are especially important for generational wealth.

The first is business ownership.

Business ownership may include operating companies, professional practices, service businesses, family enterprises, franchises, partnerships, private company shares, or entrepreneurial ventures.

Business ownership can create substantial value, but it also requires management, systems, governance, succession planning, and transferability.

The second is real estate ownership.

Real estate may include homes, rental properties, commercial buildings, land, development property, family property, or income-producing assets.

Real estate can provide stability, income, leverage, appreciation, and family identity. But it can also create conflict if heirs disagree about management, liquidity, sale, use, or maintenance.

The third is financial ownership.

This may include public equities, bonds, funds, retirement accounts, private investments, cash reserves, insurance-related assets, or other financial instruments.

Financial ownership can provide liquidity and diversification, but it still requires discipline, policy, risk awareness, and stewardship.

The fourth is intellectual property ownership.

This may include trademarks, copyrights, patents, proprietary methods, educational systems, brand assets, media libraries, licensing rights, digital assets, or institutional frameworks.

For modern wealth builders, intellectual property can become a serious ownership domain when it is protected, organized, and commercialized properly.

These four domains are not equal for every family.

Some families build through business.

Some build through real estate.

Some build through financial assets.

Some build through intellectual property.

Some combine several domains over time.

The point is not that every family must own everything.

The point is that income must eventually take an ownership form.

Ownership Must Be Identified

Ownership cannot be governed if it is not identified.

This sounds simple, but many families do not have a clear ownership inventory.

They may have assets across accounts, entities, family members, businesses, properties, informal agreements, personal records, and advisor files.

The founder may know where everything is.

But the family may not.

This creates continuity risk.

A serious ownership system should be able to answer:

What do we own?

Where is it held?

Who legally owns it?

Who controls it?

Who benefits from it?

What obligations are attached to it?

What debt exists?

What insurance exists?

What agreements govern it?

Who advises on it?

What is its purpose in the ownership system?

This is not only a financial exercise.

It is a continuity exercise.

Ownership must become visible before it can be transferred well.

Ownership Must Be Built Intentionally

Ownership formation should not be accidental.

Many families acquire assets over time without a clear ownership philosophy.

One asset is purchased because it seemed like a good opportunity.

Another is inherited.

Another is created through business.

Another is held informally.

Another is titled for convenience.

Another is placed in an entity without a broader map.

Over time, the family has assets but no system.

Intentional ownership formation asks a different set of questions:

What are we trying to build?

Which assets fit our long-term goals?

Which assets should produce income?

Which assets should preserve value?

Which assets are strategic?

Which assets are sentimental?

Which assets are too risky?

Which assets require governance?

Which assets should eventually transfer?

Which assets should be sold, consolidated, or simplified?

Ownership formation is not just accumulation.

It is disciplined conversion.

Income becomes assets.

Assets become ownership.

Ownership becomes structure.

Structure becomes continuity.

Structure: Ownership Must Become Visible

Structure is the layer that makes ownership visible.

Without structure, ownership may exist but remain difficult to understand, govern, or transfer.

This is especially important as wealth becomes more complex.

A person with one bank account and one home may not need much ownership architecture. But as a family begins to own businesses, investment accounts, multiple properties, intellectual property, trusts, private interests, insurance policies, and entity-based assets, structure becomes more important.

Structure answers the question:

How is ownership organized?

This is where ownership moves from scattered possession to deliberate architecture.

Structure Makes Ownership Visible

Visibility is one of the most important functions of structure.

When ownership is visible, a family can understand what exists.

It can see where assets sit.

It can identify who owns what.

It can clarify which assets are personal, business, investment, family, or strategic.

It can see how entities relate to one another.

It can understand how cash flows.

It can identify which documents apply.

It can coordinate advisors.

It can plan transfer more clearly.

When ownership is not visible, continuity becomes harder.

Confusion increases.

Authority becomes unclear.

Assets may be forgotten.

Responsibilities may be missed.

Heirs may misunderstand what they are receiving.

Advisors may work from incomplete information.

Conflicts may arise because family members rely on different assumptions.

Structure does not solve every problem.

But it creates a clearer ownership map.

Holding Companies as One Ownership Architecture

A holding company is one possible structure for organizing ownership.

It can sit above operating companies, real estate entities, intellectual property entities, investment assets, or future acquisitions.

Its purpose is not to magically create wealth.

Its purpose is to organize ownership.

A holding company may help clarify the difference between the ownership layer and the operating layer. It may allow multiple assets or subsidiaries to be grouped under a common ownership structure. It may help families, founders, or ownership groups think more clearly about control, cash flow, asset separation, reinvestment, and long-term ownership.

But a holding company is not automatically right for every owner.

It does not automatically create tax benefits.

It does not automatically protect assets.

It does not automatically solve succession.

It does not automatically create governance.

It does not automatically prepare heirs.

Structure should follow purpose.

That principle is essential.

The legal, tax, and operational effects of entities depend on jurisdiction, documentation, ownership design, compliance, financing, and professional implementation. Government sources like the IRS explain that business structures affect areas such as liability, taxes, registration requirements, and operational obligations, which is why structure should be selected carefully and professionally.

Trusts, Entities, Agreements, and Ownership Maps

Ownership structure may include many tools.

Trusts may hold or direct assets according to legal terms and fiduciary responsibilities.

Entities may separate operating activity, asset ownership, liability exposure, financing, management, or investment activity.

Agreements may define rights, responsibilities, voting powers, transfer restrictions, buy-sell provisions, employment rules, capital contributions, or dispute processes.

Ownership maps may show how assets, entities, owners, beneficiaries, managers, trustees, and advisors relate to one another.

Each tool has a role.

But tools are not the same as continuity.

A trust is a tool.

A holding company is a tool.

A will is a tool.

An operating agreement is a tool.

A shareholder agreement is a tool.

An ownership map is a tool.

Continuity depends on how these tools work together inside a broader ownership system.

Structure Should Follow Purpose

Structure should never be created for appearance alone.

A family should not build a complex ownership system simply to look sophisticated. Complexity without clarity can create more problems than it solves.

The right structure depends on purpose.

Is the family trying to hold real estate long term?

Transfer a business?

Separate operating risk from asset ownership?

Coordinate multiple family owners?

Prepare for succession?

Protect intellectual property?

Manage investment assets?

Create governance around shared ownership?

Support philanthropic goals?

Prepare future owners?

Different purposes may require different structures.

The principle is not “more structure is better.”

The principle is:

Clear structure should support clear ownership purpose.

Structure Without Governance Is Not Enough

Structure can make ownership visible.

But governance makes ownership functional.

This is where many families stop too early.

They create documents.

They form entities.

They establish trusts.

They organize ownership.

They consult advisors.

Then they assume the system is complete.

But if no one knows how decisions are made, how roles work, how successors are prepared, how communication happens, or how conflict is resolved, the structure may remain fragile.

Structure creates the container.

Governance creates the operating system.

Governance: Ownership Must Be Directed

Governance is the decision-making system that directs ownership.

If structure answers, “How is ownership organized?”

Governance answers, “How is ownership directed?”

This distinction matters because ownership without governance becomes vulnerable to confusion, conflict, delay, and personality-driven decisions.

Governance brings discipline to ownership.

It clarifies authority, roles, information flow, decision rights, accountability, communication, conflict resolution, succession, and stewardship standards.

For family enterprises, governance is especially important because ownership decisions are rarely only financial. They can also involve identity, family history, fairness, loyalty, emotion, control, legacy, and belonging.

This is why governance must be built intentionally.

Governance Clarifies Authority

Authority is one of the most important questions in any ownership system.

Who has the right to decide?

This may sound simple, but in family ownership systems it can become complicated.

The founder may still act like the final decision-maker even after transferring ownership.

Children may own shares but not understand their voting rights.

A trustee may have legal authority but limited family trust.

A business leader may manage operations but not own the company.

A family member may work in the business but not have authority over ownership decisions.

A nonworking owner may have economic rights but no management role.

Without clear authority, ownership decisions can become unstable.

Governance clarifies who decides, who advises, who approves, who implements, and who is informed.

This is especially important for major decisions such as:

selling a business

acquiring property

taking on debt

making distributions

hiring or removing executives

changing ownership terms

bringing family members into the business

transferring shares

reinvesting profits

changing advisors

resolving disputes

Authority should not be assumed.

It should be defined.

Governance Clarifies Roles

Family ownership systems often fail when roles are confused.

One person may be a child, shareholder, employee, board member, beneficiary, trustee, sibling, parent, executive, or advisor-facing representative.

Those roles can overlap.

But they should not be confused.

A family member may be an owner but not an employee.

A family member may be an employee but not a manager.

A family member may be a manager but not the best successor.

A family member may be a beneficiary but not a decision-maker.

A family member may be emotionally important but not qualified for operational leadership.

This is one of the hardest realities in family wealth.

Love does not automatically create role clarity.

Governance helps separate emotional belonging from ownership responsibility.

The IFC Family Business Governance Handbook identifies the multiple roles family members may hold in a family business, including owner, manager, family member, and combinations of these roles. That role complexity is one reason family businesses need governance structures rather than informal assumptions.

Governance Clarifies Communication

Communication is not a soft issue.

It is a continuity issue.

Families often lose trust when information is unclear, irregular, selective, or hidden.

Some family members may feel excluded.

Others may feel burdened.

Some may misunderstand the financial picture.

Others may assume decisions are being made unfairly.

Some may not understand why distributions are limited.

Others may not understand why reinvestment matters.

Governance creates communication rhythm.

This may include:

regular family meetings

ownership reports

financial summaries

advisor presentations

education sessions

decision memos

minutes and records

succession updates

asset reviews

risk reviews

family council communication

The purpose is not to overwhelm everyone with information.

The purpose is to create enough clarity that ownership does not depend on rumor, assumption, or selective access.

Governance Clarifies Conflict

Conflict is not a sign that governance has failed.

Conflict is one reason governance is needed.

Families disagree.

Owners disagree.

Siblings disagree.

Trustees and beneficiaries disagree.

Working and nonworking family members disagree.

Older and younger generations disagree.

Spouses and branches may see risk differently.

The problem is not disagreement.

The problem is disagreement without process.

Governance helps define how conflict will be handled before conflict becomes destructive.

This may involve mediation provisions, voting rules, family council processes, board review, advisor facilitation, buy-sell provisions, communication standards, or escalation steps.

The goal is not to eliminate emotion.

The goal is to protect ownership from being destroyed by unmanaged emotion.

Governance Keeps Ownership Coordinated

Ownership continuity depends on coordination.

As families grow and assets expand, coordination becomes harder.

More people are involved.

More decisions are required.

More assets exist.

More advisors participate.

More generations have interests.

More expectations develop.

Governance becomes the coordination system.

This is why it is central to ownership continuity.

The OECD’s corporate governance principles emphasize that governance frameworks should support transparent and fair markets, shareholder rights, disclosure, board responsibilities, and sustainability and resilience. Although the OECD principles focus heavily on corporate governance, the broader point applies to ownership continuity: durable ownership requires clear frameworks for rights, responsibilities, oversight, and decision-making.

In family ownership systems, governance also protects relationships.

It gives families a way to talk about ownership before ownership becomes a crisis.

Stewardship: Ownership Must Be Protected and Improved

Stewardship is the discipline of caring for ownership across time.

It is different from possession.

Possession says:

This is mine.

Stewardship asks:

What am I responsible for preserving, improving, and passing forward?

That shift matters.

Generational wealth cannot survive if every generation treats ownership only as personal benefit. If each generation extracts as much as possible without regard for structure, governance, risk, reinvestment, purpose, or future owners, wealth becomes vulnerable.

Stewardship creates a longer time horizon.

It asks current owners to see themselves as temporary carriers of responsibility.

They did not create every advantage they received.

They will not personally use every benefit they preserve.

They are part of a longer chain.

This is the ethical center of ownership continuity.

Stewardship Is Different From Possession

A person can possess an asset without stewarding it.

They can hold shares but ignore the company.

They can inherit property but neglect maintenance.