Contents

- 1 Overview

- 2 The Mistake Most Owners Make About Succession

- 3 What Business Succession Planning Actually Requires

- 3.1 Succession Requires Ownership Structure

- 3.2 Succession Requires Leadership Readiness

- 3.3 Succession Requires Governance

- 3.4 Succession Requires Operating Continuity

- 3.5 Succession Requires Family Communication

- 3.6 Succession Requires Successor Preparation

- 3.7 Succession Requires Financial Planning

- 3.8 Succession Requires Tax and Estate Planning

- 3.9 Succession Requires Institutional Knowledge Transfer

- 3.10 Succession Requires Board or Advisor Oversight

- 3.11 Succession Requires a Transition Timeline

- 3.12 Succession Requires an Exit or Continuity Strategy

- 3.13 Replacement Focuses on the Person

- 3.14 Transfer Focuses on the System

- 3.15 A Successor Without Transfer Is Not a Succession Plan

- 4 What Business Succession Planning Actually Requires

- 5 The Hidden Risk of Founder Dependence

- 6 The Hidden Risk of Founder Dependence

- 7 Ownership Transfer Is Not the Same as Management Transfer

- 8 Ownership Transfer Is Not the Same as Management Transfer

- 9 Family Business Succession Creates Unique Governance Challenges

- 10 The Board and Governance Role in Succession

- 10.1 Boards Help Separate Oversight From Family Dynamics

- 10.2 Advisory Boards Can Support Earlier Stage Businesses

- 10.3 Governance Bodies Help Prepare Transition

- 10.4 Outside Advisors Need Clear Direction

- 10.5 Boards Help Separate Oversight From Family Dynamics

- 10.6 Advisory Boards Can Support Earlier Stage Businesses

- 10.7 Governance Bodies Help Prepare Transition

- 10.8 Outside Advisors Need Clear Direction

- 11 Succession Planning and Business Value

- 11.1 Buyers Evaluate Transferability

- 11.2 Employees Need Confidence

- 11.3 Customers Need Stability

- 11.4 Lenders and Investors Need Continuity

- 11.5 Transferability Is a Form of Ownership Strength

- 11.6 Buyers Evaluate Transferability

- 11.7 Employees Need Confidence

- 11.8 Customers Need Stability

- 11.9 Lenders and Investors Need Continuity

- 12 The Exit Planning Problem

- 12.1 Sales is also a Form of Succession

- 12.2 Exit Planning Without Transfer Readiness Is Weak

- 12.3 Ownership Transition Must Be Prepared Before the Deal

- 12.4 Exit Planning Should Still Protect Continuity

- 12.5 Sales is also a Form of Succession

- 12.6 Exit Planning Without Transfer Readiness Is Weak

- 12.7 Ownership Transition Must Be Prepared Before the Deal

- 13 Succession Requires Prepared Successors

- 13.1 Successors Need Operating Exposure

- 13.2 Successors Need Decision-Making Practice

- 13.3 Successors Need Financial Understanding

- 13.4 Successors Need Authority Before Full Control

- 13.5 Successors Need Trust From Stakeholders

- 13.6 Successors Need Operating Exposure

- 13.7 Successors Need Decision-Making Practice

- 13.8 Successors Need Financial Understanding

- 13.9 Successors Need Authority Before Full Control

- 13.10 Successors Need Trust From Stakeholders

- 14 Succession Requires Institutional Knowledge Transfer

- 14.1 Knowledge Must Be Documented

- 14.2 Relationships Must Be Transitioned

- 14.3 Decision Logic Must Be Explained

- 14.4 The Business Must Become Less Dependent on Memory

- 14.5 Knowledge Must Be Documented

- 14.6 Relationships Must Be Transitioned

- 14.7 Decision Logic Must Be Explained

- 14.8 The Business Must Become Less Dependent on Memory

- 15 Succession Requires Family Communication

- 16 The Cost of Delaying Succession Planning

- 17 A Different Way to Think About Business Succession

- 17.1 Succession Is a Test of Ownership Maturity

- 17.2 The Founder Must Move From Control to Continuity

- 17.3 A Business That Cannot Transfer Is More Fragile Than It Appears

- 17.4 Succession Is a Test of Ownership Maturity

- 17.5 The Founder Must Move From Control to Continuity

- 17.6 A Business That Cannot Transfer Is More Fragile Than It Appears

- 18 Key Observations

- 19 Conclusion

- 20 Frequently Asked Questions

- 20.1 What is business succession planning?

- 20.2 Why is business succession planning important?

- 20.3 What is the difference between succession planning and exit planning?

- 20.4 What is the difference between ownership transfer and management transfer?

- 20.5 Why do many business succession plans fail?

- 20.6 When should a business owner start succession planning?

- 20.7 How does succession planning affect business value?

- 20.8 What role does governance play in business succession?

- 20.9 What is family business succession planning?

- 20.10 How should family businesses choose a successor?

- 20.11 Should ownership and leadership transfer at the same time?

- 20.12 What happens when some children work in the business, and others do not?

- 20.13 What is founder dependence?

- 20.14 How can owners reduce founder dependence?

- 20.15 What role does a board play in succession planning?

- 20.16 How do shareholder agreements support succession?

- 20.17 What is a buy-sell agreement?

- 20.18 How does succession planning connect to estate planning?

- 20.19 How does succession planning connect to family governance?

- 20.20 Can a business be sold as part of succession planning?

- 20.21 How does business succession support generational wealth?

- 21 Related Institute Papers

- 22 Authoritative Sources Cited in the Paper

Overview

Most owners think about business succession planning through a narrow set of questions. Who will run the business? Who will inherit the shares? Who will buy the company? When should the owner step away? What is the business worth? These questions matter, but they do not fully address the deeper succession challenge. The real issue is whether the business can survive the transfer of ownership, authority, leadership, institutional knowledge, operating responsibility, and decision-making capacity. PwC’s 2025 Family Business Survey identifies succession planning as a major concern for family firms, with 44 percent of United States family firms reporting succession planning impacts in the past year, while talent and leadership development affected 47 percent of respondents.

Business succession is the business version of continuity. In the Institute’s prior paper, Family Wealth Transfer: Why Continuity Matters More Than Inheritance, the central argument was that inheritance transfers assets, whereas continuity preserves ownership. The same principle applies to businesses. A company may transfer legally while still failing operationally. Shares may move while authority remains unclear. A successor may be named while employees, customers, lenders, advisors, and family members remain uncertain about who actually leads, makes decisions, and bears responsibility.

Succession is not only a leadership issue. It is an ownership transfer issue. A founder’s exit can expose weaknesses that were hidden while the founder remained active. The business may have been profitable, respected, and stable, but still deeply dependent on one person’s judgment, relationships, authority, memory, and instincts. When that person leaves, the business may discover that it did not have a succession plan. It had a founder. Deloitte’s family business succession work emphasizes that a well-run family enterprise needs a solid governance structure to guide the business, the family, and ownership through generational succession.

This is why business succession planning must be treated as an ownership transfer system. A serious succession plan prepares the business, the owner, the successor, the family, the ownership structure, and the governance system for transition. It does not only ask who comes next. It asks what must move, who must be prepared, what authority must be transferred, what knowledge must be documented, what relationships must be transitioned, and what structures must support continuity after the owner is no longer the central decision-maker. The International Finance Corporation’s Family Business Governance Handbook describes the many overlapping roles family business owners may hold, including owner, manager, family member, director, and combinations of these roles, which helps explain why succession is rarely a simple leadership handoff.

A business may be profitable and still succession fragile. It may have strong revenue but weak management depth. It may have loyal customers, but founder-dependent relationships. It may have valuable assets but unclear ownership rights. It may have family interest but no family alignment. It may have a successor in mind, but no transfer of authority. These are not minor issues. They determine whether a business can survive beyond the person who built it. KPMG’s Global Family Business Report states that good governance supports family business growth by creating clearer decision-making processes, reducing conflict, and supporting long-term sustainability.

Business succession planning, therefore, should not be treated as a final-stage exercise for aging owners. It should be understood as part of ownership maturity. The highest form of ownership is not merely control. It is the ability to build something that can continue when control must change hands.

The Mistake Most Owners Make About Succession

Most owners approach succession by focusing on the most visible decision: who will take over? That question feels practical because it names a person, a buyer, a child, a manager, a partner, or an outside operator. It creates the impression that succession has been addressed once a likely successor has been identified. But succession is not solved by naming someone. A successor can be named and still lack authority, preparation, clarity of ownership, employee trust, customer confidence, governance support, and access to the institutional knowledge required to lead. This is why succession planning for business owners must move beyond replacement and into transfer.

The mistake is not that owners think about successors. They should. The mistake is assuming that naming a successor means the business is prepared to transfer. A business can have a capable next leader and still fail the transition because ownership rights remain unclear, family expectations are unresolved, key relationships remain tied to the founder, or decision-making authority has not actually moved. Deloitte’s governance and succession advisory work frames family enterprises as complex systems shaped by business growth, ownership issues, family relationships, and increasing wealth, all of which create the need for structured governance and succession planning.

Succession Is Often Treated as a Replacement Problem

Succession is often treated as a replacement problem because owners naturally think in terms of roles. Who will be the next CEO? Who will manage the company? Which child is most capable? Should the business be sold to a buyer, passed to family, or transferred to management? These questions are important, but they focus too heavily on the next person. A business does not continue simply because a name appears on a document or a successor is announced. The successor must be able to lead within a system that supports them.

Replacement thinking is especially limited in founder-led businesses. A founder often does far more than occupy a formal role. The founder may carry customer trust, vendor relationships, banking relationships, pricing instincts, hiring judgment, culture, family authority, strategic memory, and crisis experience. Replacing the title does not automatically transfer those capacities. The founder’s role may be larger than the job description. That is why succession planning must ask what the founder actually holds, not only who will hold the title after the founder steps away.

A replacement plan also fails when it overlooks the needs of people around the business. Employees need to know whether leadership will remain stable. Customers need confidence that service, quality, and relationships will continue. Lenders need to know whether the business can operate without the founder. Family members need clarity about ownership, distributions, voting rights, employment, and future participation. Advisors need direction from a coordinated ownership system. Naming a successor does not answer all of these questions. Governance, structure, and preparation do.

Ownership Transfer Is Often Overlooked

Ownership transfer is often the missing layer in business succession planning. Many owners spend time thinking about management transition, but less time thinking about ownership transition. Yet management and ownership are not the same thing. A child may manage the business without owning it. A sibling may own shares without working in the business. A nonfamily executive may lead operations while the family retains ownership. A buyer may acquire ownership while the founder remains involved for a period. Each scenario creates different rights, responsibilities, expectations, and risks.

When ownership transfer is unclear, succession becomes fragile. The business may know who runs daily operations, but not who controls major decisions. Family members may know who works in the business but not how decisions about profits, voting rights, compensation, reinvestment, or sale will be handled. A successor may manage employees but lack authority over strategy. Owners may retain economic rights but lack clarity about governance. This is why the transfer of business ownership must be treated as a central part of succession planning, not as a technical matter handled after leadership has been discussed.

The International Finance Corporation’s Family Business Governance Handbook highlights how family business participants can hold overlapping roles as owners, managers, family members, and directors. That overlap is exactly why ownership transfer requires serious attention. When roles are not separated clearly, succession can create conflict because family members may confuse inheritance with leadership, employment with ownership, and family status with business authority.

The Real Question Is Whether the Business Can Survive the Transition

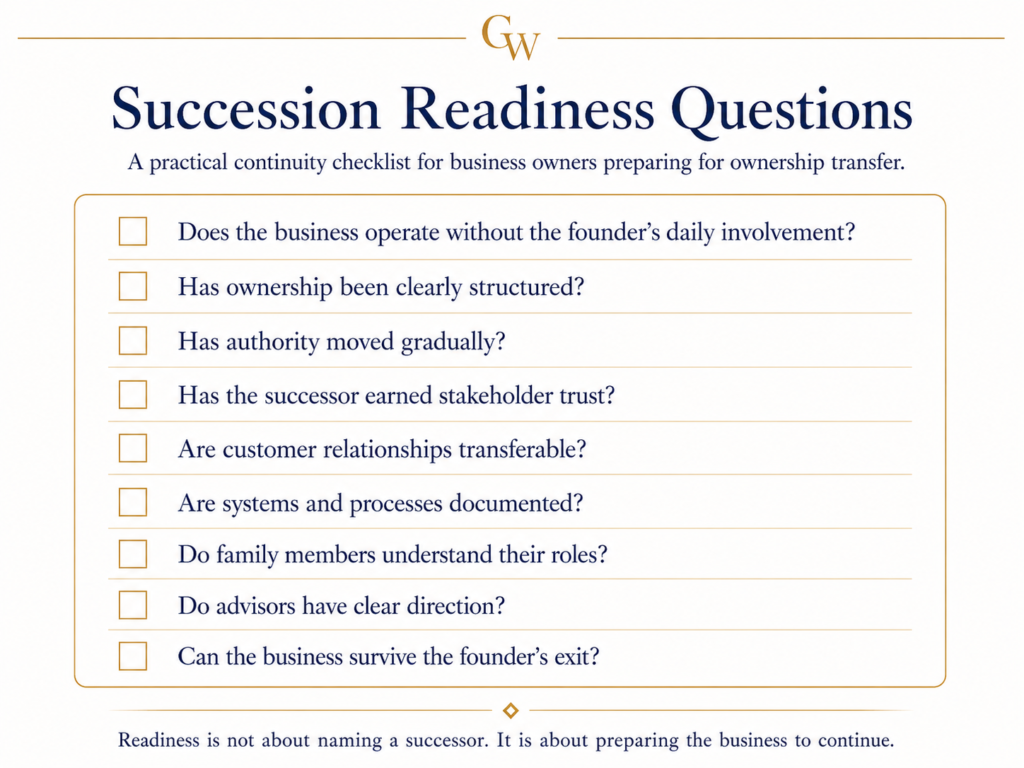

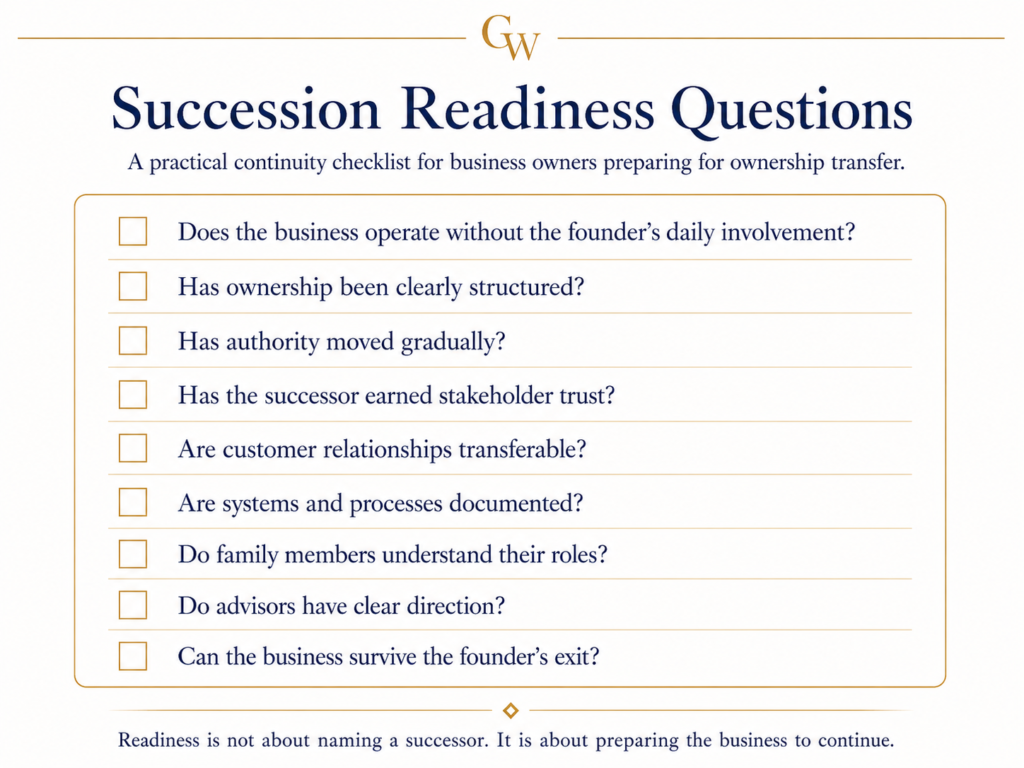

The real question in business succession planning is not only who takes over. The real question is whether the business can survive the transition. Can the company operate without the founder’s daily involvement? Can customers trust the next leader? Can employees remain confident? Can ownership transfer without confusion? Can the authority move clearly? Can the family make decisions after the founder steps back? Can lenders, suppliers, advisors, and partners continue to rely on the business?

This question changes the standard for succession. It moves the owner from replacement thinking to continuity thinking. A business that survives transition has more than a named successor. It has a prepared successor, a clear ownership structure, an operating system, documented knowledge, governance processes, stakeholder confidence, and a realistic transition path. KPMG’s 2025 Global Family Business Report notes that family businesses are increasingly expanding their view of success beyond succession toward the meaningful transition of capital across generations, which aligns with the Institute’s view that succession must include continuity, not only replacement.

This is why succession planning should begin before the owner feels ready to exit. Transition readiness is not built quickly. It requires time to prepare successors, reduce founder dependence, clarify ownership, document knowledge, develop leadership, communicate with family members, and strengthen governance. An owner who waits until illness, fatigue, conflict, market pressure, or a buyer’s offer forces the issue may discover that the business was never truly prepared to transfer. The business may have been operating, but not transferable.

Succession is not the naming of a replacement. Succession is the transfer of responsibility.

Replacement Focuses on the Person

Replacement thinking begins with a name. The owner asks who will become the next CEO, manager, president, buyer, child successor, operating partner, or outside executive. That question matters because a business needs leadership. Someone must make decisions, guide employees, communicate with customers, manage risk, and carry responsibility. But choosing a person does not automatically create a succession plan. It only identifies who may stand in the role after the current owner leaves. Deloitte’s succession guidance emphasizes that a family business transition requires planning ahead and preparing successors before the transition occurs, meaning succession depends on more than naming the next leader.

The limitation of replacement thinking is that it often treats the business as if the current owner only holds a title. In reality, many owners hold far more than a title. They may hold customer trust, employee loyalty, lender confidence, vendor relationships, pricing judgment, hiring instincts, cultural authority, family influence, and years of operating memory. The successor is not simply replacing a person in an organizational chart. The successor is being asked to inherit a working system of relationships, decisions, habits, knowledge, and authority. The IFC Family Business Governance Handbook shows why this is especially complex in family enterprises, where one person may simultaneously be an owner, manager, family member, and director.

This is why succession planning becomes weak when it stops at successor selection. A founder may say, “My son will run it,” “My daughter will take over,” “My general manager will operate the company,” or “We will sell to the right buyer.” Those statements may be directionally useful, but they do not answer the deeper questions. Has authority been transferred? Has ownership been structured? Does the successor understand the financial model? Do employees trust the next leader? Do customers believe the business will remain stable? Has the family agreed on its role after transfer? PwC’s 2025 Family Business Survey shows succession planning has affected 44 percent of United States family firms in the past year, which reinforces how central this issue has become for family-owned businesses.

Replacement focuses on who comes next. Succession requires a more serious question. What must be transferred so the business can continue? A named successor may be necessary, but the successor alone cannot carry a transition if the business remains dependent on the current owner’s relationships, authority, memory, and daily judgment. This is where business succession planning must move from the person to the system.

Transfer Focuses on the System

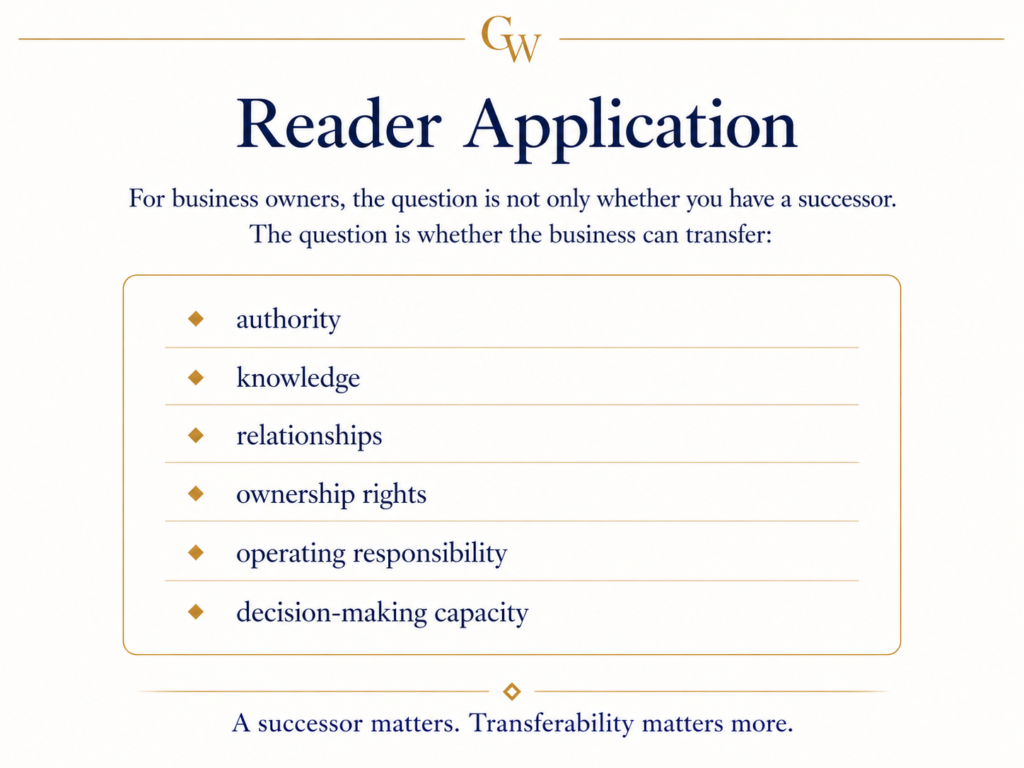

Transfer thinking begins with a different premise. It does not ask only who comes next. It asks what must move for the business to remain strong after the current owner is no longer in control. Ownership must move clearly. Authority must move intentionally. Institutional knowledge must move before it disappears. Customer trust must be transferred through exposure and relationship continuity. Employee confidence must be protected through communication and leadership readiness. Governance must support the transition so decisions do not become unclear once the founder steps back. KPMG’s Global Family Business Report identifies clear governance frameworks and effective succession planning as characteristics associated with stronger family business performance.

A business succession plan must therefore address ownership, authority, knowledge, governance, relationships, and operating capacity together. Ownership determines who holds economic, voting, control, sale, and distribution rights. Authority defines who can make decisions. Knowledge defines what the next generation or next owner must understand to operate effectively. Governance defines how decisions are made before, during, and after transition. Relationships define whether customers, employees, lenders, vendors, family members, and advisors remain confident. Operating capacity defines whether the business can function without the founder’s daily involvement. Deloitte describes family enterprises as complex because business growth, ownership issues, family relationships, and increasing wealth create the need for structured governance and succession frameworks.

This is why the transfer of business ownership cannot be treated as an administrative step after leadership selection. If shares transfer without authority, the new owner may have rights but no practical control. If authority transfers without knowledge, the successor may have power but not judgment. If leadership transfers without customer trust, revenue may become vulnerable. If management transfers occur without governance, employees may not know who truly makes the decision. If a buyer acquires the company without operating continuity, the business may lose value after closing. Transfer planning protects the business from these gaps.

Transfer also requires the owner to be honest about what the business currently depends on. Does the business depend on documented systems or on the founder’s memory? Does revenue depend on the company’s brand or on the owner’s personal relationships? Does the leadership team make decisions independently or wait for the founder? Does the family understand ownership rights, or are expectations unspoken? Does the successor have authority, or only a future possibility? These questions determine whether a succession plan is real or merely assumed.

A Successor Without Transfer Is Not a Succession Plan

A successor without transfer is not a succession plan. It is an announcement. The title may move, but the business may not. A successor can be named while the founder still controls every major decision, customers still call the founder directly, employees still seek the founder’s approval, family members still challenge the successor’s authority, and advisors still wait for the founder’s direction. In that situation, the successor may appear to be in charge, while the real decision-making authority remains with the prior owner. Deloitte’s succession planning resources emphasize that transition requires deliberate preparation rather than a last-minute leadership handoff.

This gap poses a risk to the successor and the business. The successor may be blamed for weak leadership when the deeper issue is incomplete transfer. They may be expected to lead without authority, make decisions without information, manage employees without trust, and protect ownership without governance support. The business may begin to experience uncertainty because stakeholders do not know whether the successor is truly empowered. Employees may hesitate. Customers may test the transition. Family members may question decisions. Lenders and advisors may worry about continuity. The problem is not only the successor’s readiness. It is the design of the transfer.

A serious business succession plan must be prepared for the transfer before the public transition. It must identify what the founder holds, what the successor needs, what the business must document, which relationships must be transitioned, which ownership rights must be clarified, and which governance structures must support the next stage. KPMG’s family business research notes that good governance establishes clear decision-making processes, reduces conflict, and supports long-term sustainability, which is exactly what succession requires during ownership transition.

The strongest succession plans do not only ask whether a successor has been selected. They ask whether the successor has been prepared, authorized, trusted, informed, supported, and embedded into a governance system that allows the business to continue. Naming someone without transferring responsibility creates the appearance of succession while leaving the business exposed. Succession is not the naming of a replacement. Succession is the transfer of responsibility.

What Business Succession Planning Actually Requires

Business succession planning should be understood as a system. It prepares the business, the owner, the successor, the family, the ownership structure, and the governance system for transition. A real succession plan must address ownership structure, leadership readiness, governance, operating continuity, family communication, successor preparation, financial planning, tax and estate planning, institutional knowledge transfer, board or advisor oversight, transition timing, and the owner’s exit or continuity strategy. Deloitte’s family office enterprise governance and succession work treats governance frameworks, family agreements, shareholder agreements, board effectiveness, next-generation preparation, and family office transformation as interconnected parts of long-term continuity.

The reason these components must be connected is that succession does not occur in a single place. It affects ownership, leadership, operations, family expectations, employees, customers, advisors, financing, taxes, estate structures, and long-term business value. A plan that addresses only one layer leaves the other layers exposed. For example, a leadership plan without clarity on ownership can create conflict. An ownership plan without leadership readiness can weaken operations. A tax plan without governance can move value into confusion. An exit plan without operating continuity can reduce buyer confidence. Succession planning for business owners must therefore be coordinated rather than fragmented.

Succession Requires Ownership Structure

Succession requires an ownership structure because someone must understand what is being transferred, how it is being transferred, and what rights come with it. Ownership structure may include shares, membership interests, partnership interests, operating agreements, shareholder agreements, buy-sell provisions, trusts, holding companies, family entities, voting rights, transfer restrictions, and distribution rules. These structures define who owns, who controls, who benefits, who can sell, who can vote, who can inherit, and how ownership disputes may be handled. The IFC handbook’s discussion of overlapping ownership, management, family, and director roles shows why clarity around ownership is essential in family business succession.

Ownership structure matters because leadership can change while ownership remains unclear. A child may operate the business but not own it. Siblings may own equal shares but contribute unequally. A nonfamily executive may lead the company while the family retains control. A buyer may acquire ownership while the founder remains involved temporarily. Each arrangement needs a different structure. The goal is not legal complexity for its own sake. The goal is to reduce confusion when ownership, control, economics, and responsibility begin to separate.

Succession Requires Leadership Readiness

Succession requires leadership readiness because a successor cannot become prepared at the moment the owner exits. Leadership readiness develops through exposure, responsibility, decision-making practice, financial understanding, stakeholder trust, and authority that increases over time. A successor must understand the company’s customers, employees, margins, risks, systems, vendors, culture, cash flow, and strategic choices. They must also understand the owner’s judgment, not only the owner’s instructions. Deloitte’s succession planning guidance stresses the importance of preparing successors and planning ahead for a smooth transition.

Leadership readiness also requires the current owner to make room for leadership to develop. This can be difficult because founders often remain emotionally and operationally attached to the business. They may want the successor to be ready while continuing to make every major decision themselves. That approach delays readiness. The successor needs opportunities to lead while the owner is still available to coach, correct, and transfer judgment. Leadership transfer works best when authority is gradually practiced before control fully moves.

Succession Requires Governance

Succession requires governance because transition creates decision-making pressure. Before the transition, the founder may decide most things directly. During transition, authority may become shared, contested, or unclear. After the transition, the business needs a reliable way to make decisions without depending on the founder’s presence. Governance clarifies who decides, how decisions are made, what roles owners and managers play, how family members participate, and how disagreements are resolved. This connects directly to What Is Family Governance? The Missing Layer in Most Wealth Plans.

Governance becomes especially important when ownership and management separate. Some family members may own the business but not work in it. Some executives may manage but not own. Some heirs may expect distributions but not carry operating responsibility. Some owners may want growth while others want liquidity. Governance provides the structure for these differences to be discussed without allowing every disagreement to become a business crisis. KPMG’s global family business research describes governance as crucial because it establishes clear decision-making processes, reduces conflicts, and supports long-term sustainability.

Succession Requires Operating Continuity

Succession requires operating continuity because a business must continue serving customers, paying employees, managing suppliers, producing revenue, and making decisions while ownership and leadership change. The company cannot pause because the owner is transitioning. Customers still expect service. Employees still need direction. Vendors still need communication. Lenders still need confidence. Systems still need to function. Cash flow still needs to be managed. If operations depend too heavily on the founder, succession can expose weaknesses that were hidden during normal business activity.

Operating continuity requires documented processes, management depth, reporting systems, customer transition plans, employee communication, vendor continuity, financial controls, and clear decision-making authority. It also requires the business to become less dependent on informal memory. Many businesses operate for years through habits known only to the owner. That can work until the owner is no longer available. A serious succession plan asks what must be documented, delegated, automated, professionalized, or transferred so the business can continue without disruption.

Succession Requires Family Communication

Succession requires family communication because business transition often affects more than the person who runs the company. It may affect spouses, children, siblings, inactive owners, future heirs, key employees, and family members who depend on the business economically. Silence creates risk because different people may carry different assumptions. One child may assume they will inherit leadership. Another may assume ownership will be equal. A spouse may assume the business will be sold. A sibling may assume distributions will continue. A founder may assume everyone understands the plan even when no one does.

Family communication protects both the business and the relationships around it. It gives the family a way to discuss ownership, employment, compensation, distributions, fairness, competence, leadership, sale possibilities, and future participation before transition forces those questions into conflict. PwC’s family business survey emphasizes family vision, succession planning, and leadership development as key issues for family firms, which reinforces the importance of communication before transfer becomes urgent.

Succession Requires Successor Preparation

Successor preparation is broader than leadership readiness. Leadership readiness focuses on the ability to lead the business. Successor preparation includes the broader readiness to carry responsibility inside the ownership system. The successor must understand the company, but also the family, the ownership structure, the governance process, the financial model, the tax and estate implications, the advisory team, and the expectations of stakeholders. A successor who can operate the business but cannot navigate ownership dynamics may still struggle after transition.

Successor preparation should include mentoring, education, exposure to advisors, participation in major decisions, financial training, governance education, and increasing responsibility over time. It should also include honest assessment. Not every family member who wants leadership is prepared for it. Not every capable manager understands ownership. Not every buyer can protect continuity. Preparation helps the owner distinguish desire from readiness.

Succession Requires Financial Planning

Succession requires financial planning because ownership transfer affects value, income, liquidity, taxes, debt, compensation, distributions, and the owner’s personal financial future. An owner may depend on the business for retirement income. A successor may need capital to buy in. A family may need liquidity to treat heirs fairly. A business may need cash for growth while also supporting distributions. A sale may require valuation, financing, earnouts, or seller transition terms. These issues cannot be left until the final stage of succession.

Financial planning also protects the business from being drained by transition. If the outgoing owner needs too much cash too quickly, the business may become overleveraged. If inactive owners expect distributions that the business cannot support, reinvestment may suffer. If successor compensation is unclear, resentment may build. If valuation is disputed, ownership transfer may stall. A serious succession plan must connect business value, owner needs, successor capacity, and company continuity.

Succession Requires Tax and Estate Planning

Succession requires tax and estate planning because business ownership is often one of the owner’s largest assets. The transfer of shares, membership interests, partnership interests, voting rights, estate value, insurance policies, trusts, and family entities can have legal and tax consequences. Estate planning can help address death, incapacity, liquidity, beneficiary treatment, tax exposure, and asset transfer. But tax and estate planning should not be isolated from succession. If the documents move ownership without preparing leadership and governance, the transfer may work technically while the business remains fragile.

This is one of the central lessons from Family Wealth Transfer: Why Continuity Matters More Than Inheritance. Documents can move ownership rights, but they cannot automatically transfer judgment. Tax and estate planning matter, but they become stronger when aligned with governance, leadership readiness, operating continuity, and successor preparation.

Succession Requires Institutional Knowledge Transfer

Succession requires institutional knowledge transfer because much of a business lives outside formal documents. The founder may know which customers require special handling, which vendors can be trusted, which employees are informal leaders, how pricing decisions are made, when cash flow tightens, which risks are hidden, and which opportunities are worth pursuing. If that knowledge remains trapped in the owner’s memory, the business becomes vulnerable when the owner exits.

Institutional knowledge transfer should be intentional. It may include documenting processes, creating operating manuals, building customer records, explaining pricing logic, introducing successors to lenders and vendors, recording decision principles, and helping future leaders understand why certain choices were made. The goal is not to remove judgment from the business. The goal is to make judgment transferable.

Succession Requires Board or Advisor Oversight

Succession requires board or advisor oversight when the business has grown beyond what informal founder control can safely manage. A board, advisory board, ownership council, family council, trustee group, CPA, attorney, banker, consultant, or outside advisor can help bring discipline to the process. Oversight helps owners ask better questions, evaluate successor readiness, prepare governance structures, and protect the business from emotional or reactive decisions. KPMG’s family business research identifies formal boards and governance as important contributors to stronger decision-making and long-term sustainability.

Outside advisors can be valuable, but they need clear direction. Advisors cannot replace ownership governance. If the family is divided, advisors may receive conflicting instructions. If the owner has not clarified goals, advisors may optimize technical pieces without supporting the larger continuity plan. Advisor oversight works best when the business and family have a clear governance framework.

Succession Requires a Transition Timeline

Succession requires a transition timeline because transfer rarely happens well as a single, sudden event. The owner may need time to reduce involvement. The successor may need time to build authority. Employees may need time to adjust. Customers may need repeated exposure to the next leader. Lenders and vendors may need confidence in continuity. Family members may need time to understand the ownership structure. A timeline helps move succession from intention to execution.

The timeline should identify stages. What happens now? What responsibilities move first? When does the successor begin leading meetings? When are customer relationships transitioned? When does ownership transfer? When does the founder stop making daily decisions? When does the board or advisory group begin oversight? Without a timeline, succession remains vague. With a timeline, the business can prepare deliberately.

Succession Requires an Exit or Continuity Strategy

Succession requires an exit or continuity strategy because not every owner wants the same outcome. Some owners want the business to remain in the family. Some want to sell to children, employees, management, partners, strategic buyers, private buyers, or investors. Some want to stay involved as chair, advisor, landlord, shareholder, or mentor. Some want a full exit. Each path requires different planning. Exit planning and succession planning are connected because both involve the transfer of ownership, authority, and responsibility.

A continuity strategy asks how the business will survive beyond the current owner. An exit strategy asks how the owner will step away while protecting value, relationships, and future stability. The best plans often address both. They prepare the business to continue and prepare the owner to transition. A business that can continue without the owner is usually stronger, whether the owner transfers it to family, sells it to management, or exits through an outside sale.

Replacement Focuses on the Person

Replacement thinking begins with a name. The owner asks who should become the next CEO, president, general manager, buyer, child successor, operating partner, or outside executive. That question matters because every business needs leadership. Someone must make decisions, guide employees, manage customers, protect cash flow, and carry responsibility. But naming one person does not automatically create a business succession plan. It only identifies a possible successor. Deloitte’s succession guidance emphasizes that a smooth transition requires planning ahead, selecting the right candidates, and preparing successors before the transition occurs.

The weakness of replacement thinking is that it treats the owner’s role as merely a formal position. In many founder-led businesses, the owner holds far more than a title. The founder may hold customer trust, employee loyalty, vendor relationships, lender confidence, hiring judgment, pricing logic, strategic memory, family authority, and the ability to resolve problems that were never written down. The successor is not simply stepping into a job description. The successor is being asked to inherit a network of relationships, habits, decisions, and operating knowledge that may still live inside the founder. The IFC Family Business Governance Handbook explains that family business participants often hold overlapping roles as owner, manager, family member, and director, which is why succession is rarely a simple personnel change.

A replacement plan can create the appearance of progress while leaving the business exposed. The owner may say that a child will run the company, a general manager will take over, a buyer will eventually acquire the business, or a professional operator will be hired. Those statements may point in a useful direction, but they do not answer the harder succession questions. Has authority moved? Has ownership been structured? Has the successor earned trust? Do employees know who decides? Do customers believe the business will remain stable? Does the family understand its role after transition? PwC’s 2025 Family Business Survey reports that succession planning affected 44 percent of United States family firms in the past year, which reflects how central this issue has become for family-owned companies.

Replacement focuses on who comes next. Succession requires a more serious question: what must be transferred so the business can continue? A named successor may be necessary, but the successor alone cannot carry a transition if the business still depends on the current owner’s relationships, authority, judgment, memory, and daily involvement. This is why business succession planning must move from the person to the system.

Transfer Focuses on the System

Transfer thinking begins with the whole business, not only the next leader. It asks what must move for the company to remain strong after the current owner is no longer the center of control. Ownership must move clearly. Authority must move intentionally. Institutional knowledge must move before it disappears. Customer trust must be transitioned through exposure and relationship continuity. Employee confidence must be protected through communication and leadership readiness. Governance must support the transition so decision-making does not become unclear once the founder steps back. KPMG’s Global Family Business Report states that good governance supports growth by creating clear decision-making processes, reducing conflict, and strengthening long-term sustainability.

A serious succession plan must address ownership, authority, knowledge, governance, relationships, and operating capacity together. Ownership defines economic rights, voting rights, control rights, distribution rights, sale rights, and transfer restrictions. Authority defines who can make decisions and where the limits sit. Knowledge defines what the next leader or ownership group must understand to operate wisely. Governance defines how decisions are made before, during, and after transition. Relationships determine whether customers, employees, lenders, vendors, advisors, and family stakeholders remain confident. Operating capacity determines whether the business can function without the founder’s daily involvement. Deloitte’s family enterprise work connects business growth, ownership issues, family relationships, and increasing wealth with the need for structured governance and succession frameworks.

This is why the transfer of business ownership cannot be treated as a technical step after leadership selection. If shares transfer without authority, the new owner may have rights but no practical control. If authority transfers without knowledge, the successor may have power but not judgment. If leadership transfers without customer trust, revenue may become vulnerable. If management transfers occur without governance, employees may not know who truly makes the decision. If a buyer acquires the company without operating continuity, the business may lose value after closing. Transfer planning protects the business from these gaps.

Transfer also requires the owner to be honest about what the business currently depends on. Does the business depend on documented systems or on the founder’s memory? Does revenue depend on the company’s brand or on the owner’s personal relationships? Does the leadership team make decisions independently or wait for the founder? Does the family understand ownership rights, or are expectations still unspoken? Does the successor have authority now, or is it only a future possibility? These questions determine whether a succession plan is real or merely assumed.

A Successor Without Transfer Is Not a Succession Plan

A successor without transfer is not a succession plan. It is an announcement. The title may move, but the business may not move with it. A successor can be named while the founder still controls every major decision, customers still call the founder directly, employees still seek the founder’s approval, family members still question the successor’s authority, and advisors still wait for the founder’s direction. In that situation, the successor may appear to be in charge while the real decision-making system remains attached to the prior owner. Deloitte warns that when the older generation expects continuity without giving the next generation room to lead, it can reduce authority and weaken the desire to take leadership roles.

This gap creates risk for both the successor and the business. The successor may be blamed for weak leadership when the deeper issue is incomplete transfer. They may be expected to lead without authority, make decisions without information, manage employees without trust, and protect ownership without governance support. The business may begin to experience uncertainty because stakeholders do not know whether the successor is truly empowered. Employees may hesitate. Customers may test the transition. Family members may challenge decisions. Lenders and advisors may question continuity. The problem is not only the successor’s readiness. It is the design of the transfer.

A serious business succession plan must prepare the transfer before the public transition. It must identify what the founder holds, what the successor needs, what the business must document, what relationships must be transitioned, what ownership rights must be clarified, and what governance structures must support the next stage. Naming someone without transferring responsibility creates the appearance of succession while leaving the business exposed. Succession is not the naming of a replacement. Succession is the transfer of responsibility.

What Business Succession Planning Actually Requires

Business succession planning should be understood as a system. It prepares the business, the owner, the successor, the family, the ownership structure, and the governance system for transition. A real succession plan addresses ownership structure, leadership readiness, governance, operating continuity, family communication, successor preparation, financial planning, tax and estate planning, institutional knowledge transfer, board or advisor oversight, a transition timeline, and a clear exit or continuity strategy. Deloitte’s global succession guidance states that a well-run family enterprise is grounded by governance that guides the business, family, and ownership through generational succession.

The reason these components must be connected is that succession does not happen in one place. It affects ownership, leadership, operations, family expectations, employees, customers, suppliers, lenders, advisors, taxes, estate structures, and long-term business value. A plan that addresses only one layer leaves the other layers exposed. A leadership plan without ownership clarity can create conflict. An ownership plan without leadership readiness can weaken operations. A tax plan without governance can move value into confusion. An exit plan without operating continuity can reduce buyer confidence. Business succession planning must therefore be coordinated, not fragmented.

Succession Requires Ownership Structure

Succession requires ownership structure because someone must understand what is being transferred, how it is being transferred, and what rights come with it. Ownership structure may include shares, membership interests, partnership interests, operating agreements, shareholder agreements, buy-sell provisions, trusts, holding companies, family entities, voting rights, transfer restrictions, and distribution rules. These structures help define who owns, who controls, who benefits, who can sell, who can vote, who can inherit, and how ownership disputes may be handled. The IFC handbook shows why this matters by describing the overlapping roles family business participants may hold as owners, managers, family members, and directors.

Ownership structure matters because leadership can change while ownership remains unclear. A child may operate the business but not own it. Siblings may own equal shares but contribute unequally. A nonfamily executive may lead the company while the family retains control. A buyer may acquire ownership while the founder remains involved for a transition period. Each arrangement needs a different structure. The goal is not legal complexity for its own sake. The goal is to reduce confusion when ownership, control, economics, and responsibility begin to separate.

Poor ownership structure creates succession risk because business authority and economic rights can move in different directions. One person may be responsible for performance while another controls voting rights. One family branch may rely on distributions while another wants reinvestment. One successor may lead operations while inactive owners expect influence. These are not only legal questions. They are ownership continuity questions. A business succession plan must make ownership clear enough for the company to continue after the founder is no longer available to interpret everyone’s role.

Succession Requires Leadership Readiness

Succession requires leadership readiness because the next leader cannot become prepared at the moment authority moves. Leadership readiness develops through exposure, responsibility, decision-making practice, financial understanding, stakeholder trust, and gradual authority. A successor must understand the company’s customers, employees, margins, risks, systems, vendors, culture, cash flow, and strategic choices. They must also understand the owner’s judgment, not only the owner’s instructions. Deloitte’s succession guidance stresses the importance of preparing successors before the transition occurs.

Leadership readiness also requires the current owner to make room for leadership to develop. This is often difficult because founders are emotionally and operationally attached to the business. They may want the successor to be ready while continuing to make every major decision themselves. That approach delays readiness. The successor needs opportunities to lead while the owner is still available to coach, correct, and transfer judgment. Leadership transfer works best when authority is practiced before full control moves.

A business should therefore assess readiness before transition, not after. Can the successor lead meetings? Can they handle difficult employees? Can they speak with customers? Can they understand financial reports? Can they make tradeoffs between growth, risk, cash flow, and reinvestment? Can they work with advisors? Can they earn the confidence of lenders and suppliers? These questions should not be answered by hope. They should be answered through repeated exposure to real responsibility.

Succession Requires Governance

Succession requires governance because transition creates decision-making pressure. Before the transition, the founder may decide most things directly. During transition, authority may become shared, contested, or unclear. After the transition, the business needs a reliable way to make decisions without depending on the founder’s presence. Governance clarifies who decides, how decisions are made, what roles owners and managers play, how family members participate, and how disagreements are resolved. This connects directly to What Is Family Governance? The Missing Layer in Most Wealth Plans. KPMG’s 2025 family business research states that governance is crucial because it establishes clear decision-making processes, reduces conflict, and supports long-term sustainability.

Governance becomes especially important when ownership and management separate. Some family members may own but not work in the business. Some executives may manage but not own. Some heirs may expect distributions without carrying operating responsibility. Some owners may want growth while others want liquidity. Governance provides the structure for these differences to be discussed without allowing every disagreement to become a business crisis. In this sense, governance is not bureaucracy. It is the decision-making infrastructure that allows succession to hold.

Governance also protects the successor. A successor who steps into a business without governance may become trapped between founder expectations, family emotions, employee uncertainty, and ownership confusion. A successor who steps into a governed system has clearer authority, clearer reporting, clearer decision rights, and a better chance of leading with legitimacy. The transition is still difficult, but it is no longer dependent only on personality.

Succession Requires Operating Continuity

Succession requires operating continuity because the business must continue serving customers, paying employees, managing suppliers, producing revenue, and making decisions while ownership and leadership change. The company cannot pause while the owner transitions. Customers still expect service. Employees still need direction. Suppliers still need communication. Lenders still need confidence. Systems still need to function. Cash flow still needs to be managed. If operations depend too heavily on the founder, succession can expose weaknesses that were hidden during normal business activity.

Operating continuity requires documented processes, management depth, reporting systems, customer transition plans, employee communication, vendor continuity, financial controls, and clear decision-making authority. It also requires the business to become less dependent on informal memory. Many businesses operate for years through habits known only to the owner. That can work until the owner is no longer available. A serious succession plan asks what must be documented, delegated, automated, professionalized, or transferred so the business can continue without disruption.

Institutional memory is part of operating continuity. The business needs to preserve why certain customers are handled differently, why certain pricing decisions are made, which vendors can be trusted, which employees have informal influence, what risks typically arise in certain seasons, and how the owner thinks through difficult trade-offs. Without that transfer, the successor may inherit operations without inheriting the logic behind operations.

Succession Requires Family Alignment

Succession requires family alignment when the business is owned, influenced, or expected to benefit multiple family members. This becomes especially important when some family members work in the business and others only own it. Working family members may believe they deserve more compensation, authority, or control because they carry daily responsibility. Nonworking owners may believe they deserve equal economic benefit because they share ownership. Parents may want fairness among children while the business requires competence, discipline, and clear authority. PwC’s 2025 Family Business Survey highlights the importance of family vision, succession planning, and leadership development in family firms, which reflects the need for alignment before transition.

Family alignment does not mean every family member agrees on everything. It means the family has discussed enough to understand the business, ownership structure, leadership plan, and the expectations for each role. It means family members understand the difference between employment, ownership, management, governance, inheritance, compensation, and distributions. Without that clarity, succession can turn business decisions into family disputes.

A family business succession plan must therefore address both the emotional and structural aspects of the transition. The family must know who will lead, who will own, who will work, who will receive distributions, how inactive owners will receive information, and how disagreements will be addressed. If these questions remain unspoken, the transition may not fail because the business is weak. It may fail because the family never aligned around ownership.

The Hidden Risk of Founder Dependence

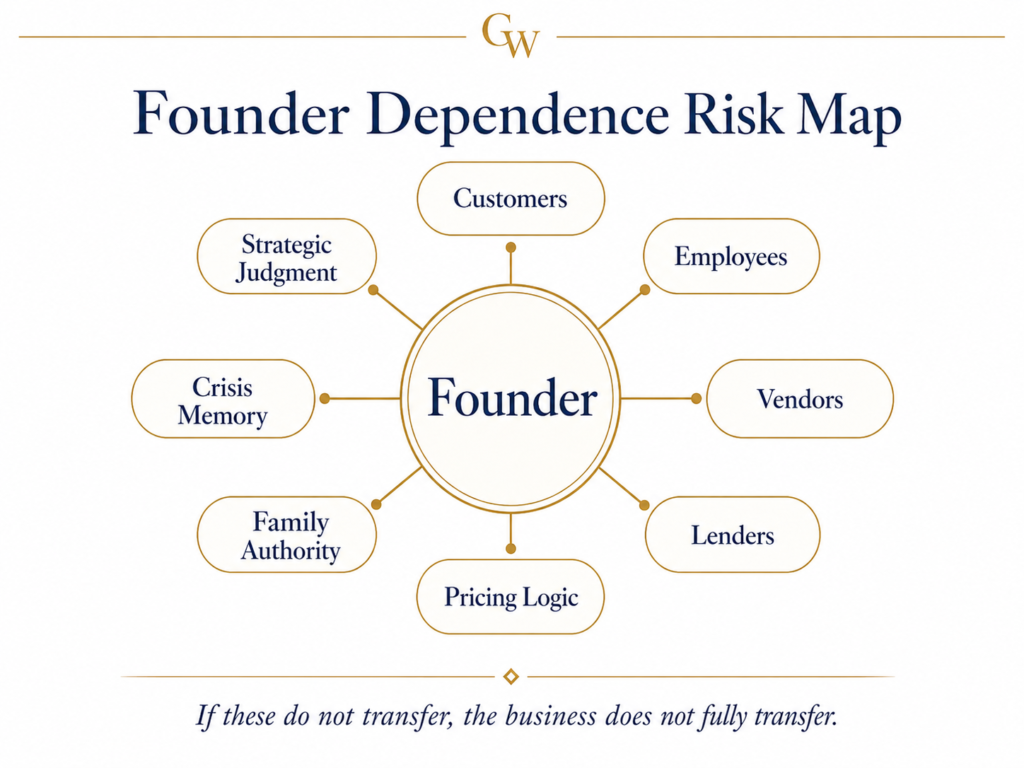

Founder dependence is one of the most serious risks in business succession planning because it often hides inside success. The business may look strong while the founder is active. Revenue may be growing. Customers may be loyal. Employees may be stable. Vendors may be responsive. Banks may be comfortable. The family may believe the company is durable. But beneath that apparent strength, the business may still depend heavily on one person’s relationships, pricing judgment, hiring instincts, banking trust, vendor history, operating memory, family authority, and strategic intuition. When the founder exits, the business may lose more than a leader. It may lose the operating center.

Founder dependence makes a business harder to transfer, value, sell, and continue. Buyers, lenders, successors, employees, and family members all need confidence that the business can operate without the founder. If too much personal value is tied to the owner, the transition becomes more dangerous. The company may still be profitable, but its transferability is weaker than the financial statements suggest. Deloitte’s succession guidance notes that current leaders play a significant role in setting the tone for transition, and that failure to give the next generation real authority can weaken continuity.

Founder Knowledge Is Often Undocumented

Founder knowledge is often undocumented because the founder has carried the business for years through memory, instinct, and experience. The founder may know how to price work, which customers require special handling, which vendors can solve urgent problems, which employees need closer supervision, which risks appear before they show up in reports, and which opportunities are worth pursuing. That knowledge may be essential to the company, but it may not exist in any system the successor can use.

Undocumented knowledge creates transition risk. When the founder is present, the business can function because the knowledge is available within one person. When the founder exits, the successor must recreate what was never transferred. That can lead to slower decisions, weaker customer service, missed risks, operational mistakes, and loss of confidence. A serious succession plan should document processes, decision logic, customer history, vendor relationships, pricing principles, reporting systems, and operating rhythms before the founder steps away.

The goal is not to remove judgment from the business. The goal is to make judgment transferable. A company becomes more durable when its knowledge is no longer trapped in one person’s memory. This is one of the most practical ways an owner can increase the transferability of their assets before succession.

Founder Relationships Are Often Nontransferable Unless They Are Intentionally Transitioned

Founder relationships can be one of the most valuable and fragile parts of a business. Customers may buy because they trust the founder. Lenders may extend credit because they know the founder’s character. Vendors may provide flexibility because of years of relationship. Employees may stay because of personal loyalty. Advisors may understand the company mainly through the founder’s explanations. These relationships often feel stable until the founder leaves.

Relationships do not transfer automatically. The successor must be introduced, trusted, tested, and gradually accepted. Customers need to see the successor in meaningful conversations before the founder exits. Employees need to experience the successor making decisions. Lenders and vendors need confidence that the business remains competent. Advisors need to know who will provide direction after the transition. If these relationships are not transitioned intentionally, succession may weaken the very trust that kept the business stable.

A strong succession plan treats relationship transfer as part of operating continuity. It creates a deliberate process for introducing the successor to customers, employees, vendors, lenders, community partners, advisors, and family stakeholders. The founder’s credibility becomes a bridge, not a permanent dependency.

Founder Authority Often Masks Weak Governance

Founder authority often masks weak governance because a single strong owner can make unclear systems appear functional. The founder decides. The founder resolves conflict. The founder communicates with advisors. The founder approves spending. The founder handles family tension. The founder interprets ownership rights. The founder tells employees what matters. While the founder is active, this can appear efficient. After the founder exits, the weakness becomes visible.

The problem is not that the founder had authority. Founder authority is often necessary in the early stages of a business. The problem is when the business never develops a decision-making system beyond the founder. If no one knows who decides after the founder, governance was never built. If family members do not understand ownership roles, governance was never built. If managers wait for the founder before acting, governance was never built. If advisors receive conflicting directions after the transition, governance was never built.

This is why succession must include governance before the founder leaves. Governance turns personal authority into organizational clarity. It helps the business and family know who decides, how decisions are made, what requires approval, and how conflict is handled. Without governance, the founder’s exit does not simply remove a person. It removes the decision-making system.

Founder Dependence Can Reduce Business Value

Founder dependence can reduce business value because transferable businesses are generally stronger than owner-dependent businesses. A buyer wants to know whether revenue will continue after the founder leaves. A lender wants confidence that management can operate without disruption. Employees want stability. Customers want continuity. Family successors need systems they can inherit. If the business depends too heavily on the founder’s personal relationships, memory, and daily control, the company may be riskier than its financial performance suggests.

This matters whether the owner plans to sell, transfer to family, promote management, or retain ownership while stepping back. In every scenario, the business must prove it can function beyond the founder. If it cannot, succession becomes harder. Sale value may decline. Transition risk may increase. Successors may struggle. Family conflict may rise. Employees may leave. Customers may become uncertain. The issue is not only continuity. It is valuable.

Reducing founder dependence is therefore one of the most important acts of ownership maturity. The owner must build management depth, document knowledge, transition relationships, clarify authority, strengthen governance, and prepare successors before the business is forced into transition. A business that can operate without the founder is more transferable, more valuable, and more likely to survive succession.

The Hidden Risk of Founder Dependence

Founder dependence is one of the most serious risks in business succession planning because it often hides inside success. The business may look strong while the founder remains active. Revenue may be stable. Customers may be loyal. Employees may trust the company. Vendors may respond quickly. Banks may feel comfortable. The family may believe the business is durable. But beneath that surface, the business may still depend heavily on one person’s customer relationships, pricing logic, hiring judgment, banking trust, vendor history, operating memory, family authority, and strategic instincts.

When the founder exits, the business may lose more than a leader. It may lose the operating center. That is the real danger. The founder may not simply be the person at the top. The founder may be the person who explains the numbers, calms customers, negotiates terms, reads employee dynamics, remembers every exception, handles family tension, and makes decisions no one else has been trained to make. Deloitte’s family business succession guidance emphasizes that a smooth transition requires planning ahead and preparing successors in advance, because leadership continuity cannot be improvised at the moment of transfer.

Founder dependence makes a business harder to transfer, value, sell, and continue. A business that cannot operate without the founder may be profitable, but it is not fully transferable. Buyers want confidence that revenue, employees, customers, and operations will remain stable after the owner exits. Lenders want confidence that the company can repay its debt without relying on a single person’s judgment. Successors need systems they can inherit. Employees need clarity about who leads next. BDC describes succession and exit planning as a way to support continuity and enhance business value, whether ownership is sold externally or transferred to family or management.

Founder Knowledge Is Often Undocumented

Founder knowledge is often undocumented because many owners build businesses through experience before they build formal systems. They know how the business works because they have lived inside it for years. They know which customers need careful handling, which vendors can be trusted, which employees are informal leaders, which numbers require attention, which risks appear before they become visible, and which decisions require patience. The business may have accounting records, customer lists, contracts, and operational tools, but the real operating judgment may still live inside the founder’s memory.

This includes unwritten systems, pricing logic, customer history, vendor habits, operating judgment, and crisis memory. The founder may know why one customer receives different terms, why one supplier gets priority, why one product line is more fragile than it looks, why certain expenses should not be cut, or why a specific employee should not be promoted too quickly. These details may not appear in the financial statements, but they often shape how the business actually survives. The IFC Family Business Governance Handbook emphasizes that family businesses must plan for succession and begin grooming the next leaders if the business is to survive into the next stage.

When this knowledge is not transferred, the successor inherits operations without inheriting the logic behind operations. That can lead to weaker pricing, slower decisions, damaged customer relationships, vendor confusion, employee instability, and avoidable mistakes. The issue is not that the successor lacks intelligence. The issue is that the business failed to transfer the founder’s accumulated judgment before the founder stepped back.

A serious succession plan should convert founder memory into institutional knowledge. This may include documented processes, customer notes, pricing principles, vendor records, decision histories, risk explanations, operating manuals, financial dashboards, and repeated conversations about why the founder makes certain decisions. The goal is not to remove human judgment from the business. The goal is to make enough judgment transferable that the business can continue without depending on one person’s memory.

Founder Relationships Are Often Nontransferable

Founder relationships are often nontransferable unless they are intentionally transitioned. Customers may trust the founder personally. Lenders may extend confidence because they know the founder’s character. Suppliers may offer flexibility because the relationship has been built over the years. Employees may remain loyal because of personal history. Advisors may understand the company mainly through the founder’s interpretation. Community trust may be tied more closely to the owner’s reputation than to the business as an institution.

These relationships may feel stable while the founder is present. They become fragile when the founder leaves without preparing others to carry them. A customer may stay loyal to the founder but hesitate with the successor. A lender may become cautious when the person they trusted is no longer involved. A vendor may stop offering informal flexibility. Employees may begin questioning whether the business is still the same company. Advisors may become uncertain about who has the authority to speak for ownership. Harvard Business Review has noted that failed CEO succession can disrupt employees, damage reputation, erase value, and weaken the legacies of the outgoing leader, the board, and the successor.

Relationship transfer must therefore be part of succession planning. A successor should not meet key customers only after the founder exits. Lenders should not learn about the next leader only when a financing issue arises. Employees should not be introduced to the successor’s authority only after the founder disappears. Suppliers, advisors, partners, and community stakeholders need gradual exposure to the next leadership system.

The founder’s credibility should become a bridge, not a permanent dependency. The strongest founders use their authority to transfer trust. They bring successors into customer meetings. They allow the next leader to speak. They introduce lenders and suppliers to their successors. They let employees experience the successor making real decisions. This process does not diminish the founder. It strengthens the business by institutionalizing relationships rather than personalizing them.

Founder Authority Often Masks Weak Governance

Founder authority often masks weak governance because one strong owner can make unclear systems appear functional. The founder decides. The founder resolves disputes. The founder approves spending. The founder handles difficult employees. The founder negotiates with banks. The founder interprets family expectations. The founder communicates with advisors. The founder decides what the business can afford, who gets promoted, what gets reinvested, and which risks matter. While the founder remains active, this can look efficient.

The weakness appears when the founder is no longer available. If no one knows who decides after the founder, governance was never fully built. If employees wait for the founder before acting, authority was never truly distributed. If family members disagree about ownership rights, expectations were never clarified. If advisors received conflicting instructions, decision-making was never coordinated. KPMG’s family business research finds that strong governance leads to clearer decision-making, reduces conflict, and supports long-term sustainability.

The problem is not that the founder had authority. Founder authority is often necessary in the early stages of a business. The problem is when the business never matures beyond the founder’s authority. A business cannot rely forever on one person’s ability to interpret every conflict, approve every major decision, and hold every relationship together. At some point, personal authority must become governance.

Governance turns founder control into decision-making continuity. It clarifies who decides, what requires approval, how owners participate, how managers are evaluated, how family members receive information, and how disagreement is handled. Without governance, the founder’s exit does not simply remove a person. It removes the system that the business has been using to make decisions.

Founder Dependence Can Reduce Business Value

Founder dependence can reduce business value because a buyer, lender, successor, or investor must ask whether the business can continue without the owner. A business that depends too heavily on one person may look profitable but still carry transfer risk. Revenue may be tied to the founder’s relationships. Margins may depend on the founder’s pricing instincts. Employee retention may depend on personal loyalty. Financing may depend on a bank’s confidence in the founder. Operations may depend on habits no one else understands. The more the business depends on the founder, the less transferable it becomes.

This affects buyer confidence. A buyer does not only purchase past performance. A buyer evaluates whether future performance can continue after the change in ownership. If the business has weak management depth, undocumented systems, customer relationships tied to the founder, unclear governance, or unstable leadership succession, the buyer may view the business as riskier. Exit Planning Institute materials similarly emphasize that reducing owner dependency improves a company’s value, scalability, longevity, and attractiveness to potential buyers.

Founder dependence also affects lender confidence and employee stability. Lenders want to know that cash flow and management discipline can survive the transition. Employees want to know that the business has a real future. Successors want authority, information, and systems that allow them to lead. Family members want confidence that the business will not weaken because one person stepped away. If these stakeholders do not believe the company can function beyond the founder, the succession plan becomes fragile.

Reducing founder dependence is one of the most important acts of ownership maturity. It requires management depth, documented knowledge, transferable relationships, clear authority, governance structures, financial reporting, and successor development. A business that can operate without the founder is usually stronger, more transferable, and more likely to survive an ownership transition.

Ownership Transfer Is Not the Same as Management Transfer

Ownership transfer is not the same as management transfer. This distinction is essential because many business succession plans become fragile when owners confuse management responsibility with ownership rights. A child may manage the business but not own it. A sibling may own shares but not work in the business. A nonfamily executive may run operations while the family retains ownership. A buyer may acquire ownership while the founder remains involved for a temporary transition period. These are different transitions, and each one requires a different structure.

Management transfer moves operating responsibility. Ownership transfer moves economic rights, control rights, voting rights, distribution rights, sale rights, and long-term ownership authority. These two transitions can happen together, but they do not have to. In some businesses, the next manager becomes the next owner. In others, the next manager is a professional executive while ownership remains with the family. In some cases, ownership transfers to children who do not work in the company. In others, ownership transfers to a buyer while management remains in place. CIBC describes business succession planning as determining how business ownership will transfer and how the owner will transition out of a management role, which reinforces that ownership and management are connected but distinct issues.

Confusing these roles creates conflict. A child who manages the business may assume they deserve control because they carry daily responsibility. A sibling who does not work in the business may still expect equal ownership benefits. A nonfamily executive may need authority to lead but may not have ownership rights. A founder may transfer management but continue influencing decisions informally. A buyer may own the business but still rely on the founder’s relationships during transition. Without clarity, succession can lead to resentment, uncertainty, and poor decision-making.

Management Transfer Moves Operating Responsibility

Management transfer concerns who runs the business. It includes responsibility for employees, customers, vendors, operations, sales, service delivery, execution, reporting, hiring, culture, systems, and day-to-day accountability. A management successor must understand how the business works operationally. They must know how revenue is produced, how employees are led, how customer issues are handled, how cash flow is protected, and how decisions are made under pressure.

Management transfer can occur within the family, within the existing leadership team, or through an external executive. A daughter may become president. A long-time general manager may become chief executive. A professional operator may be hired. A management team may buy the company or run it under family ownership. In each case, the central question is whether the person leading operations has the capability, authority, and trust needed to manage the business.

But management responsibility alone does not answer ownership questions. The manager may not control shares. They may not decide on distributions. They may not determine whether the company is sold. They may not have final authority over capital allocation, ownership structure, or major governance decisions. That is why management transfer must be coordinated with ownership transfer. Otherwise, the person responsible for performance may lack the authority required to lead.

Ownership Transfer Moves Economic Rights and Control